Why Low Online Share Markets Deliver the Fastest Growth

Mature markets often dominate headlines, but early-stage markets represent untapped potential. The numbers show why they should not be overlooked.

eCommerce: Video Gaming

Learn about global gaming ecommerce companies, revenues, and distribution.

Nadine Koutsou-Wehling

Data Journalist

August 13, 2024

Market Trends

Online gaming stays a favorite pastime for consumers, and market revenues are growing way past pandemic highs. The reason for this is simple: Video games are a favorite distraction for many.

Here is what there is to know on video gaming eCommerce.

Video games are typically not included in ECDB’s definition of online markets. ECDB’s market data includes the sale of physical goods over the internet. But games are nowadays mostly consumed through downloads or cloud gaming on mobile devices.

This analysis considers video games that are distributed online, as well as downloads to game consoles or PCs. In-scope are mobile games, pay-to-play games, and browser games that require in-game purchases. Network or cloud gaming is included, but hardware games, taxes and in-game advertising are excluded.

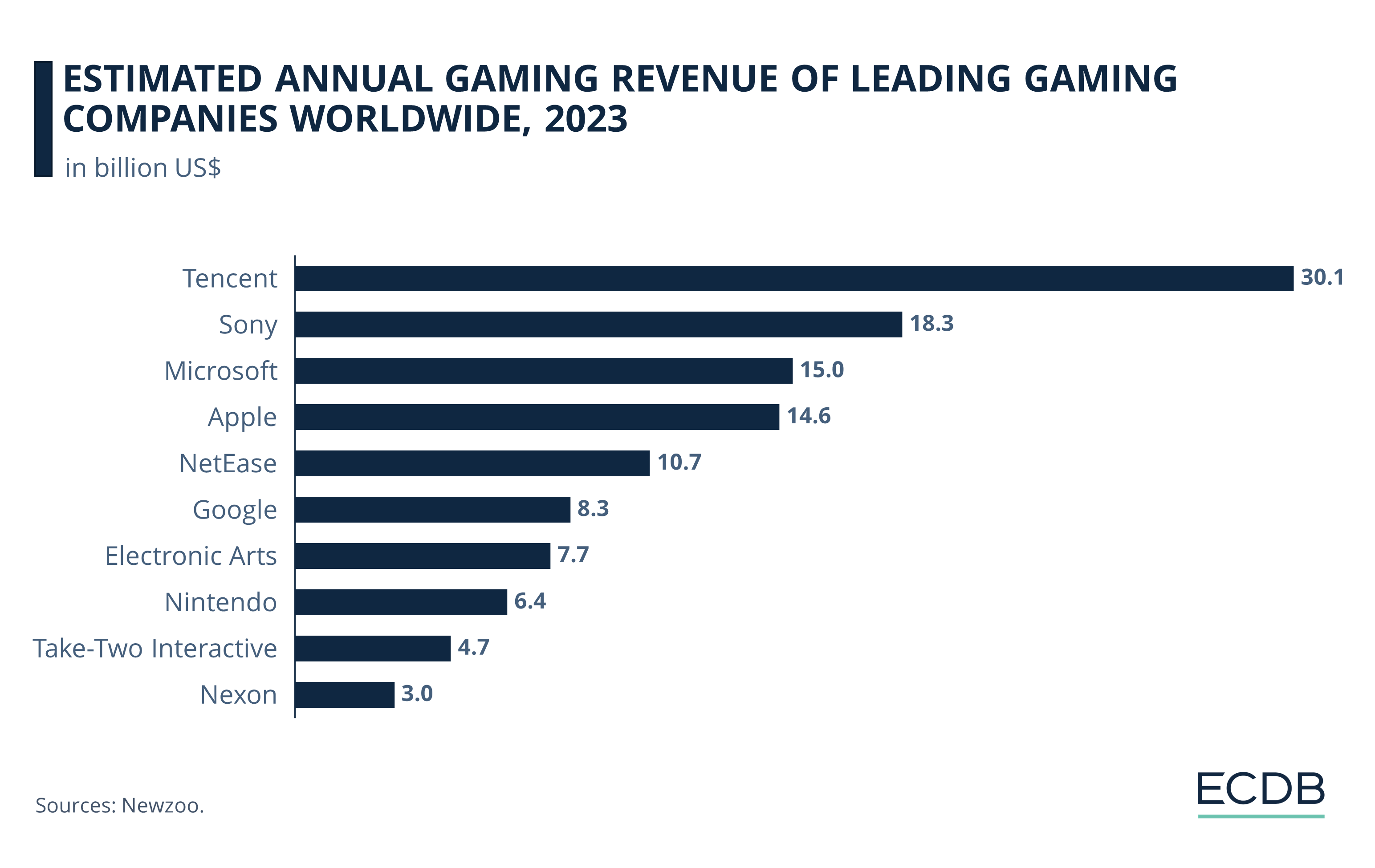

Newzoo compiled a list of leading gaming companies by revenue:

Tencent generated gaming revenues of US$30.1 billion in 2023.

The Chinese multinational conglomerate company owns the League of Legends franchise, which is one of the most popular games in the world. It is free to play, but players can purchase cosmetic items called skins to customize the appearance of their characters.

Second with revenues of US$18.3 billion in 2023.

Sony drove sales over the past few years with the release of its latest console, the PlayStation 5 in November 2020. It also owns the game selling platform, PlayStation Store, and manages subscriptions like PlayStation Plus.

Microsoft climbed to third position in 2023.

This is in no small part due to its acquisition of Activision Blizzard, which ranked 7th in 2022.

Apple made gaming revenues of US$14.6 billion.

The company has recently placed increasing weight on the playability of its products, advertising, and continuously new product versions.

NetEase ranks fifth with revenues of US$10.7 billion.

Microsoft renewed NetEase's agreement with Blizzard to bring popular titles like World of Warcraft and Hearthstone back to China. This renewed partnership will see numerous Blizzard games returning to the Chinese market.

In sixth place is Google with 2023 gaming revenues of US$8.3 billion, followed by EA with US$7.7 billion. Further behind are Take-Two Interactive (US$4.7 billion) and Nexon (US$3 billion).

Note that all 10 companies on this list have annual revenues in the billions of dollars, indicating the immense profitability of the gaming industry. Considering that this is just one branch of the whole industry, we move on to the next category: video game distribution platforms.

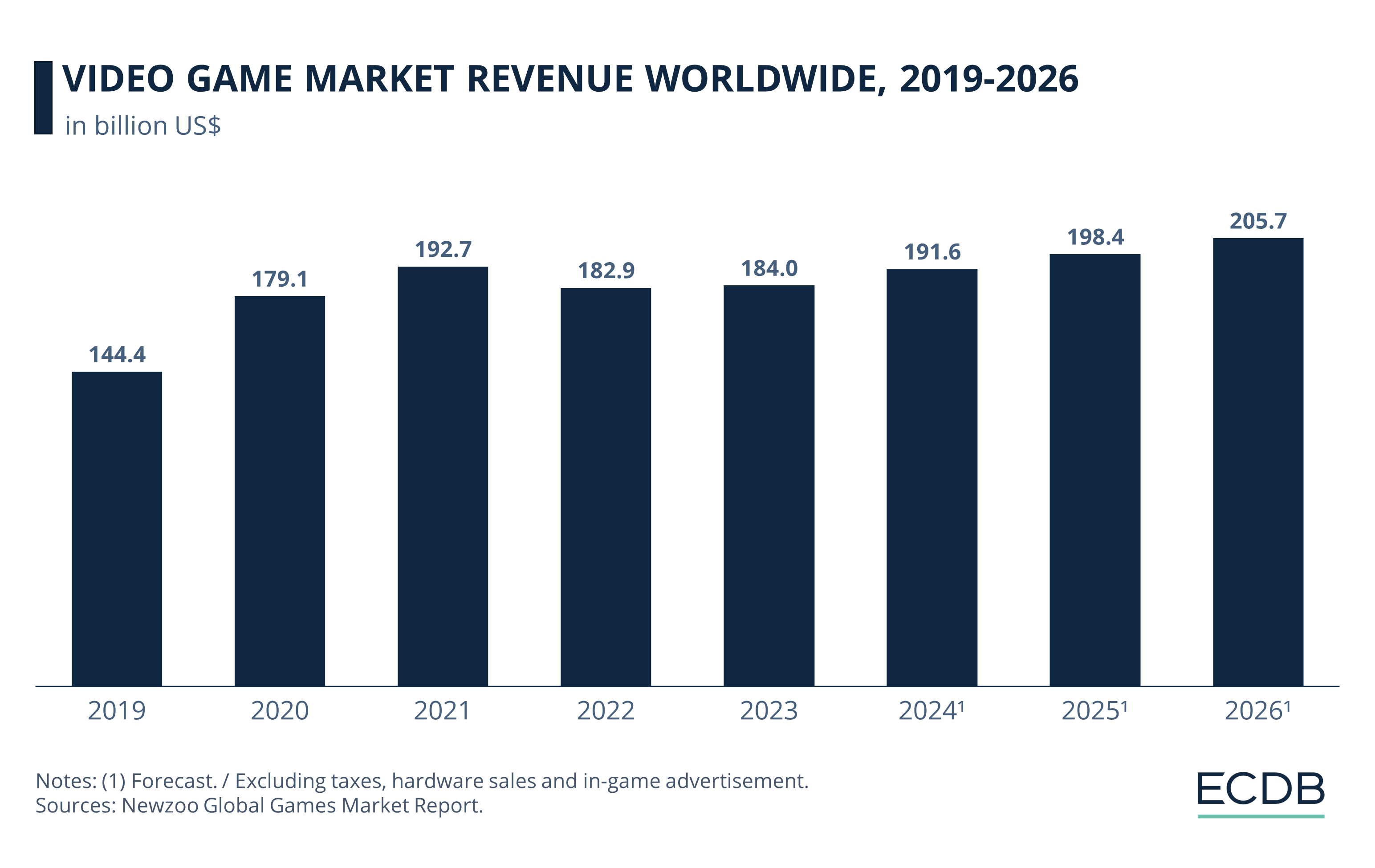

According Newzoo’s Global Games Market Report, video game revenues are expected to surpass US$200 billion by 2026. US$200 billion is roughly what a small-scale European economy generates in a year.

Market value was at US$144.4 billion in revenue by 2019.

Revenues continued to grow throughout the pandemic to US$192.7 billion in 2021.

Despite post-pandemic losses, the gaming market recovered quick to generate US$184 billion in 2023.

It is expected that the market will continue to grow over the next three years, although it may not be as pronounced as it was during the global health crisis.

Ultimately, the video games market is forecast to reach US$205.7 billion by 2026.

Gaming was perfect for pandemic consumers. But there were revenue losses after governments lifted bans and consumers went outside again. Despite slowdowns, however, gaming stays a popular hobby.

Let’s get into further details.

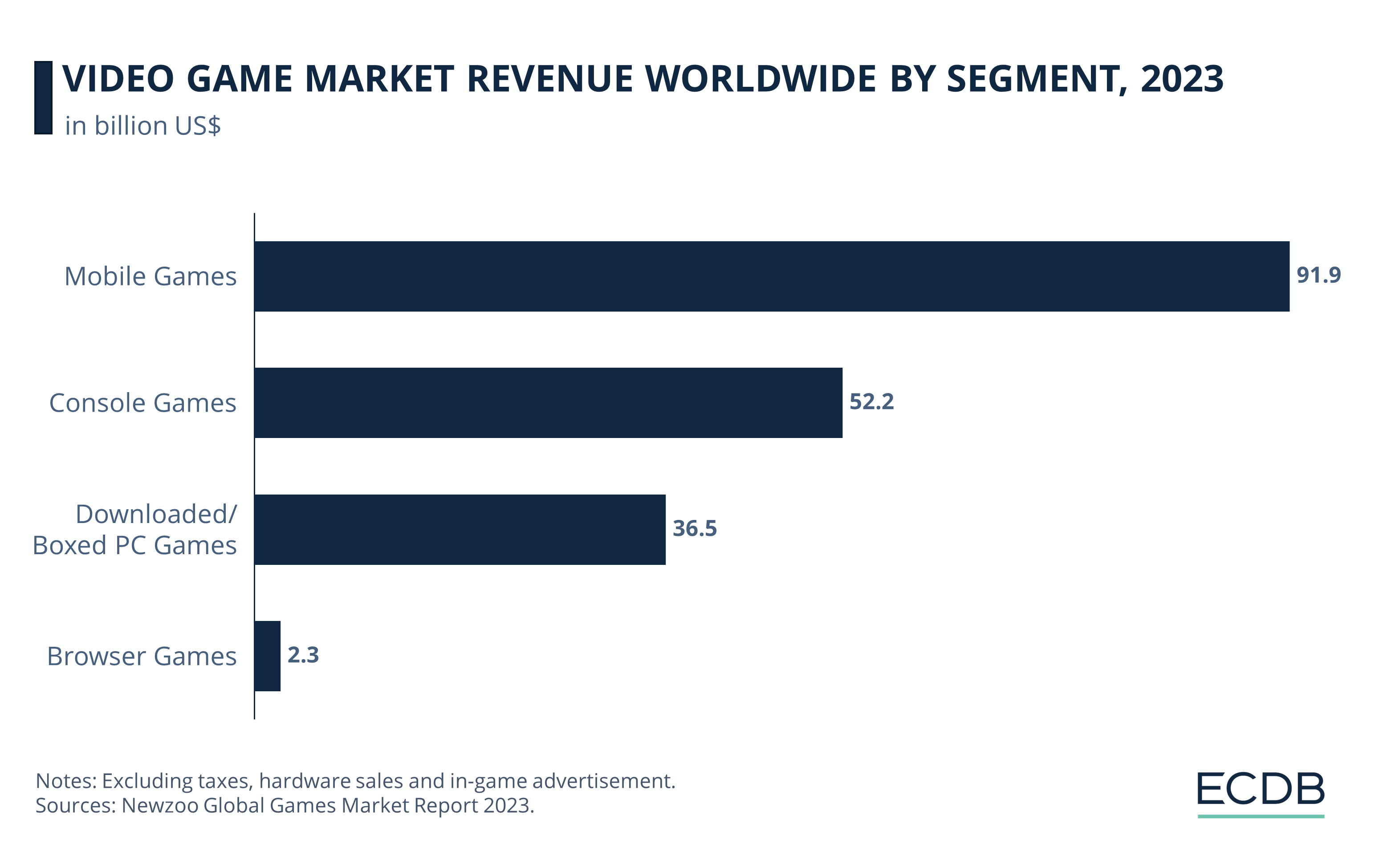

There are different types of distribution platforms for online games that determine where and how players interact with the product. Each distribution type generates revenue differently, and while some methods are more common, others are niche.

Here is how each segment is performing.

Mobile has the highest share of the video gaming market. In 2023, mobile games generated US$91.1 billion, which is nearly 50% of total market revenues.

The easy access of mobile games is a likely reason for their popularity, as they can be bought by anyone with a smartphone or tablet. They also provide a fun distraction on public transport or during waiting times and short breaks.

Other categories like console games and downloaded/boxed PC games, are experiencing losses. Sources cite the decline is caused by disrupted gaming development schedules during the pandemic, so people shifted to mobile games that were available and cheap.

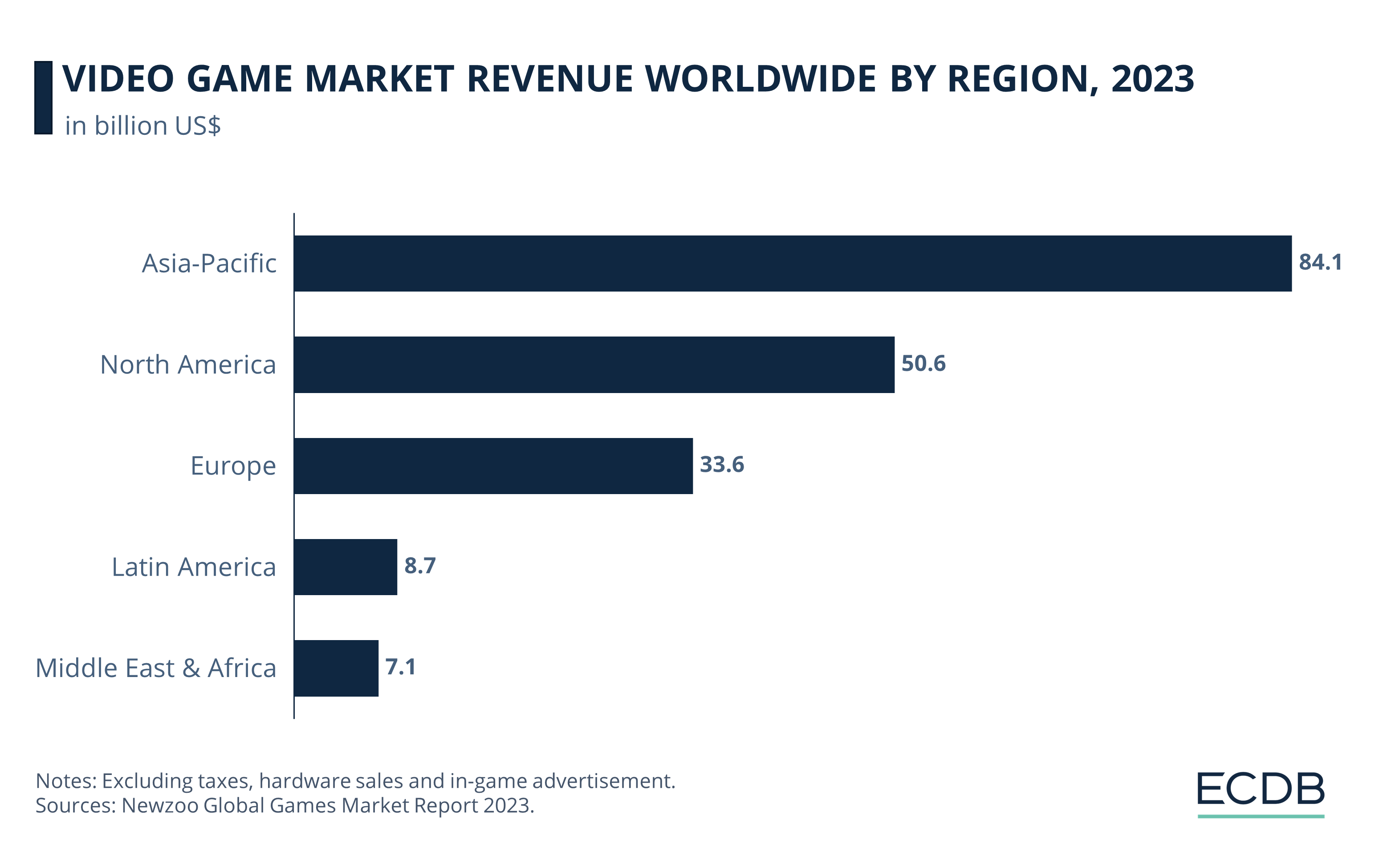

Gaming is a universal hobby. Revenues are highest in Asia-Pacific, but market growth has stalled in recent years. The Chinese government imposed playtime limitations for underaged consumers in 2021, which likely had a lasting impact on consumption rates.

Asia Pacific gaming generated revenues of US$84 billion in 2023, compared to US$50.6 billion in North America.

Europe saw US$33.6 billion. Latin America and Middle East & Africa have lowest revenues.

First, it pays to know the distinction between video game development companies and game distribution services. While game businesses can fall into both categories, they describe different aspects of the industry.

Game developing companies are involved in the design, development, and sometimes the publishing of games. They are responsible for creating the game's content, graphics, sound, and gameplay. Game distribution services, on the other hand, are platforms that host and distribute games developed by these companies or by independent developers. Big companies like Sony or Microsoft do both things. With big success!

Most game sales today are made through digital distribution services. Even physical retailers tend to offer mostly game cards and codes that can be used on these platforms, some of which are:

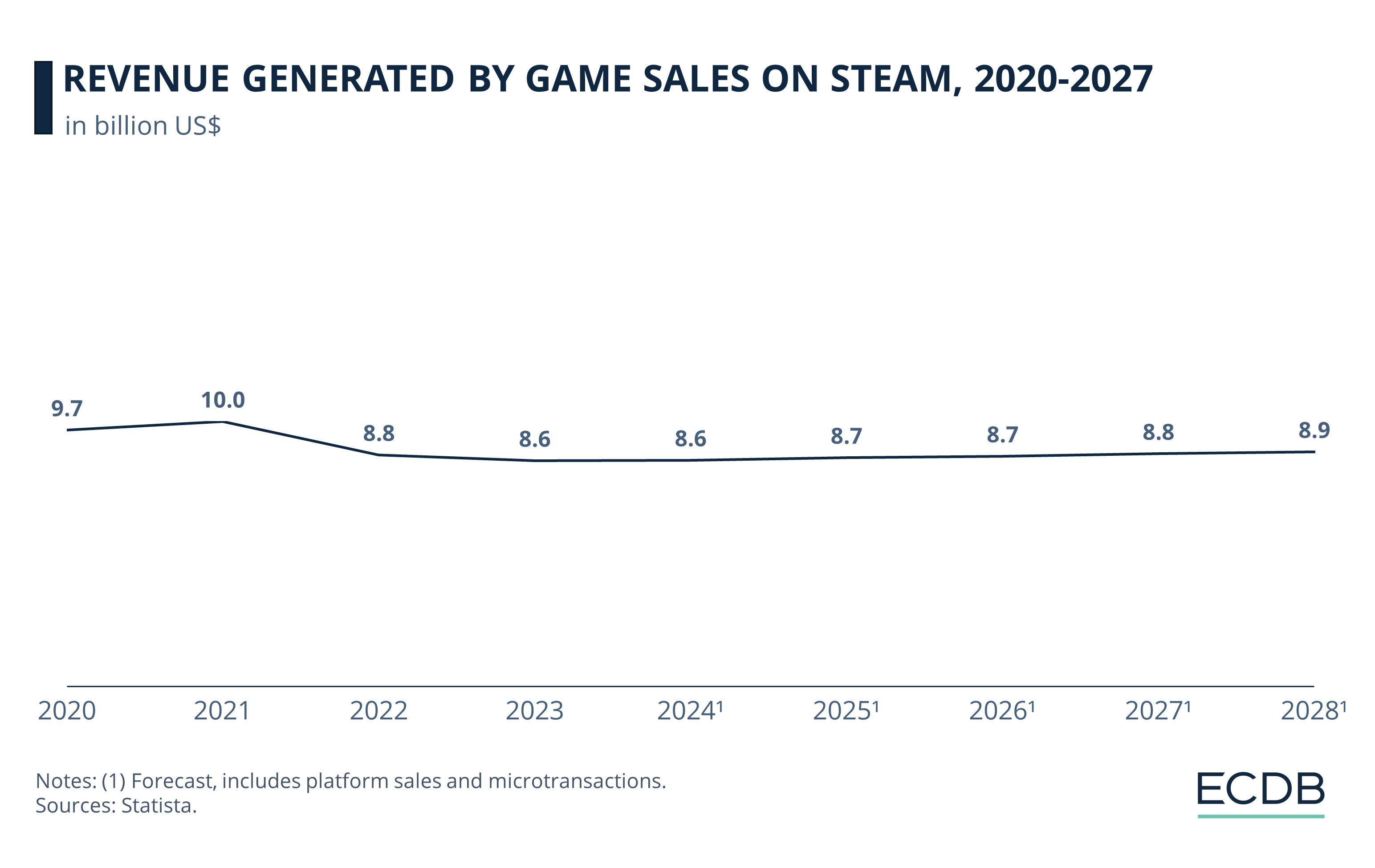

Steam is considered the largest game distribution service. The platform hosts thousands of games and new releases, excluding games from competitors that are limited to their own distribution services like Sony, Microsoft or CDPROJEKTRED. There are some Valve games that can only be accessed through Steam, such as Dota 2, the Left 4 Dead series, and Counter Strike.

Below is a chart depicting past and projected game sales revenue on Steam from 2020 to 2028.

Other popular digital distribution platforms include:

Green Man Gaming: This smaller platform gained popularity through a competitive pricing strategy and rewards programs, including rewards for purchases, trade-ins, referrals, and game reviews.

GamersGate, a Swedish digital distributor, is similar in size and strategy to Green Man Gaming, and also offers incentives, discounts, and rewards programs.

GOG.com, formerly Good Old Games, is a Polish distribution service. Having started out as a digital download platform for classic PC games, it now also provides new releases. GOG.com offers a money-back guarantee, additional downloadable content, and a loyal following of classic game enthusiasts.

Origin is Electronic Arts' distribution platform, launched in 2011 as a competitor to Steam. It contains some third-party games, a large catalog of older EA titles, and exclusive popular EA game titles.

Amazon offers new releases, online digital codes that can be used in Steam, and discounts. However, it lacks older titles and re-released classics.

Epic Games is a U.S. company, founded in 1991. The company is best known for one of the world's largest games, Fortnite, as well as Unreal Engine.

The online video games market has gained substantial ground in recent years. Despite positive expectations for growth, external factors can impact the industry, which in recent years were rising prices through inflation and microchip shortages, and new legislation like the one implemented by the government in China to reduce user times.

In the meanwhile, the number of online gamers is climbing by the year. Statista estimates that the number of global users in the Games segment is 2.6 billion in 2024. The figure is expected to increase until 2029. Thus, projections for the video gaming market are optimistic, also because of increasing innovation for consumers.

Related Articles

Mature markets often dominate headlines, but early-stage markets represent untapped potential. The numbers show why they should not be overlooked.

In February, global e-commerce reached revenues of US$370.1 billion, marking a further decline from the previous month. But in a year-on-year perspective, February 2026 revenues weren't so bad at all. Here are the details.

Europe is outpacing the Americas in e-commerce growth right now. Here is why the continent proves more resilient than expected, despite a challenging macroeconomic outlook.

Click here for

more relevant insights from

our partner Mastercard.

Our Tool

We’re not just another blog—we’re an advanced e-commerce data analytics tool. The insights you find here are powered by real data from our platform, providing you with a fact-based perspective on market trends, store performance, industry developments, and more.

Analyze retailers in depth with our extensive Retailer dashboards and compare up to four retailers of your choice.

Learn More

Combine countries and categories of your choice and analyze markets in depth with our advanced market dashboards.

Learn More

Compile detailed rankings by category and country and fine-tune them with our advanced filter options.

Learn More

Discover relevant leads and contacts in your chosen markets, build lists, and download them effortlessly with a single click.

Learn More

Benchmark transactional and conversion funnel KPIs against market standards and gain insight into the key metrics of your relevant market.

Learn MoreOur reports provide pre-analysed data and highlight key insights to help you quickly identify key trends.

Learn More

Find your perfect solution and let ECDB empower your e-commerce success.