When we talk about Europe’s South at ECDB it is mostly to contrast its eCommerce markets with those of the continent's leading online economies. But today’s news is more positive than that. ECDB predicts growth rates for Southern European eCommerce markets that exceed world averages.

Apart from the statistical reality that smaller markets tend to achieve higher growth because less revenue is needed to bring about significant percentage increases, other factors must be considered. They encompass both international and domestic influences.

Top Growth Rates Impacted by International Platforms

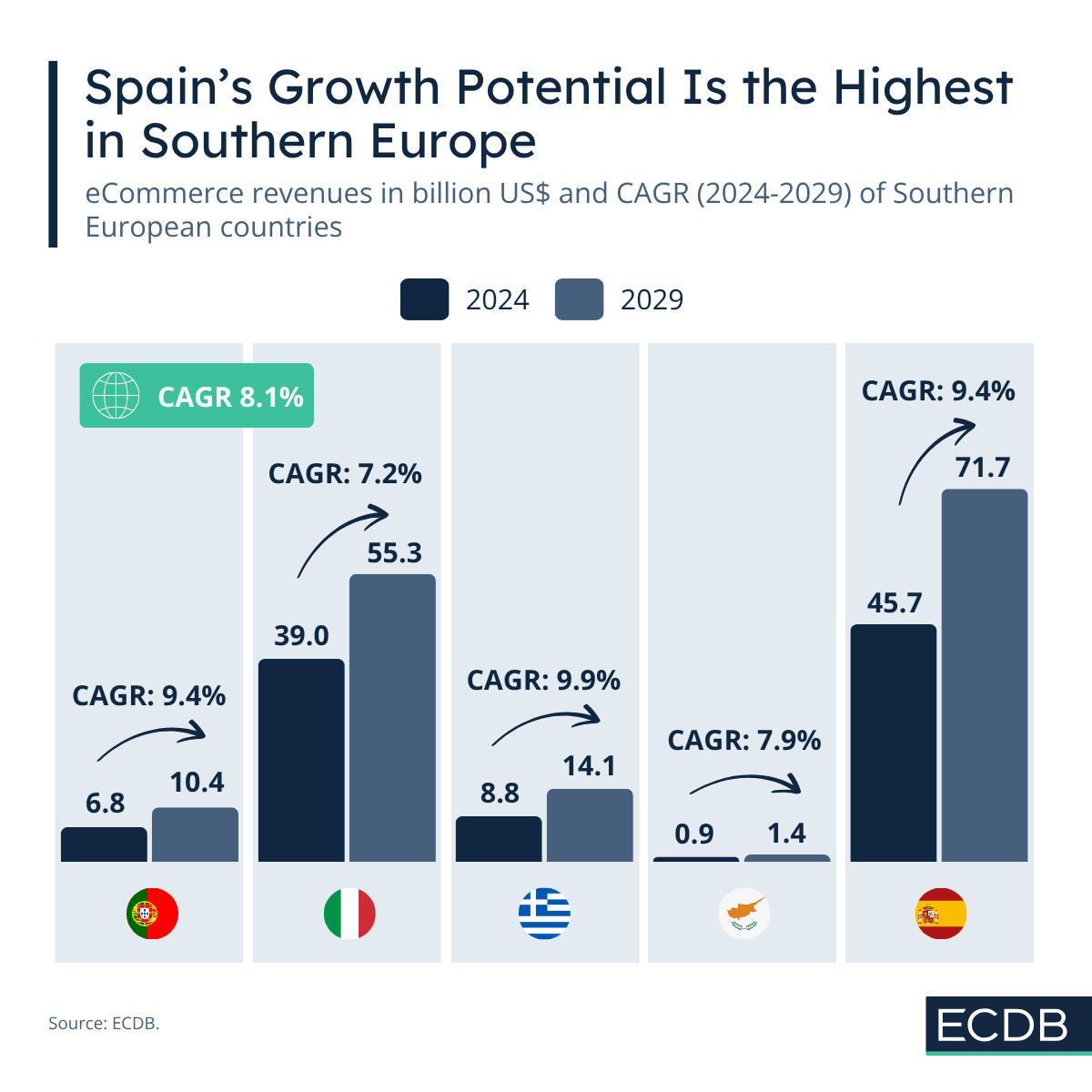

Spain, Portugal and Greece are at the top ranges of CAGR (2024-2029) value predictions. Other than some of the leading markets in the world, this puts them at an advantage over world averages. The global CAGR for the period between 2024 and 2029 is at 8.1%. Greece exceeds that figure most notably with a CAGR of 9.9%, followed by Spain and Portugal with 9.4%.

These above-average rates are largely due to the expansion phase of the three markets. It is particularly being fueled by the international marketplaces which are thriving globally at the moment. Among them are TikTok Shop, AliExpress and Temu. Spain was one of the first European markets in which TikTok Shop launched, and the other two rank in the top five of all three markets.

There are several reasons for their splash in the respective markets. Their low-cost, wide-assortment strategy is popular globally, but especially in markets plagued by economic crises and stagnant real wages. In markets where eCommerce has had a slower trajectory, the emergence of international marketplaces has helped kick off a development formerly based on apps that connect local small businesses to users online.

For the discerning online shopper, price is the number one consideration. Low-cost platforms have not only hit that particular nerve of consumers, but have also accelerated the development of eCommerce in countries where it was previously underdeveloped.

Domestic Players Support Lasting Growth in Regions

International eCommerce platforms undoubtedly play a significant role, but domestic players also have an important impact. They are more similar in Spain and Portugal due to proximity than they are in Greece.

In Spain and Portugal, Inditex and El Corte Inglés are the driving forces of eCommerce development. Inditex has its various domains with a global reach and competitive strategies. El Corte Inglés has the recognition among consumers and delivery capabilities to compete with even the biggest in the game. It is in partnership with Alibaba since 2018.

Greece is a curious case. Greek eCommerce lacks its own Amazon domain due to the challenging landscape for the services usually offered by the eCommerce giant. While not impossible, it would be unprofitable to invest heavily in the infrastructure changes needed to provide the standardized experience for which the Amazon brand is known. Consequently, local companies such as Skroutz, Public, and regional supermarkets dominate Greek eCommerce.

They drive projected eCommerce development as well, because of their enhanced experience and reach over the years. This kind of evolution is more demanding, but also more lasting than development driven by international platforms.

Italy and Cyprus Have Lower Predicted CAGRs for Different Reasons

Italy and Cyprus are two Southern European markets with a CAGR below the global average (2024-2029). Despite their similar status, the reasons differ greatly.

Cyprus has a special status because of its geography and history: Split into two parts, a Greek part and a Turkish part, as well as governed by British influence for a time, its allegiances are unclear, and so are its logistical responsibilities and economic affiliations. As an island state, Cyprus is not easily accessible for international trade, which affects its growth trajectory. Its CAGR is projected at 7.9% between 2024 and 2029.

Italy does not have these issues preventing it from participating in the global online economy. Still, its projected CAGR (2024–2029) is the lowest among the considered countries, at 7.2%.

The underlying reasons for Italy’s subpar expected development are demographic and a widespread preference for offline channels in key categories like fashion, which are usually core revenue drivers. Italy, Germany, and the DACH region as a whole are predicted to have lower economic growth rates in the coming period.