Electronics Is the Biggest E-Commerce Category in the US. Meet the Top Retailers Behind It.

Electronics is not just consumer tech, as the top 100 retailers in the US market show. Here is who's behind the United States' largest category.

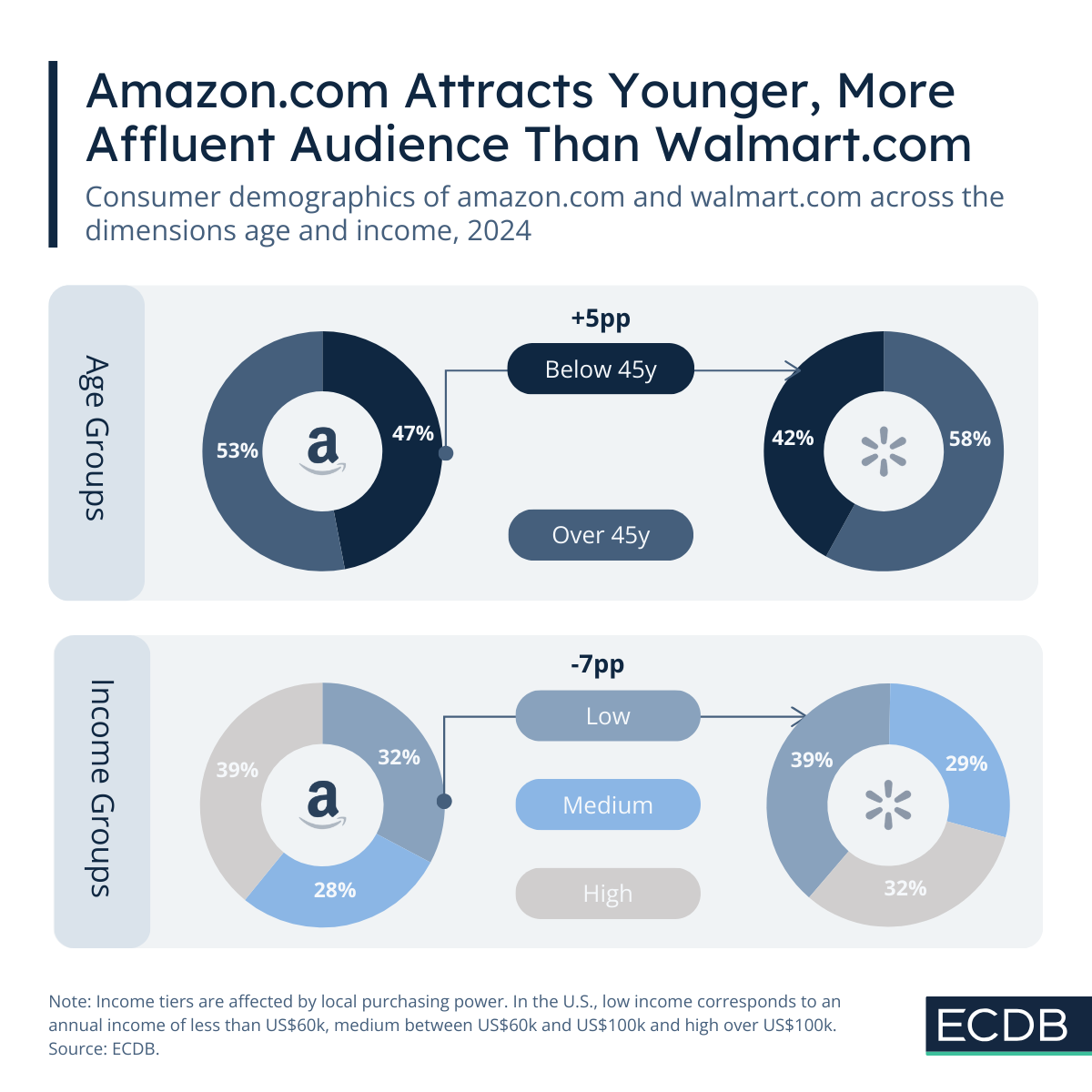

Customer Demographics on Amazon.com and Walmart.com

Comparing customer demographics of retailers at ECDB shows that some serve specific consumer segments, while others are more balanced. Amazon appeals to a broad range of users, but some patterns emerge.

Nadine Koutsou-Wehling

Data Journalist

October 28, 2025

Retailers

Amazon.com and Walmart.com are at the top of United States eCommerce, with no other domestic company coming close to their billions of dollars in GMV. While Amazon remains the undisputed number one, Walmart’s online domain has been catching up over recent years.

In that sense, it is worth knowing who shops at these two retailers. In how far do online shoppers at walmart.com and amazon.com resemble one another, and how do they differ?

Here’s what ECDB’s Customer Demographics section has to say about it.

Across two dimensions, age and income, amazon.com and walmart.com are generally quite balanced. Amazon is the more evenly distributed retailer among the two, speaking to its broad appeal throughout the general consumer base.

The highest-earning income group, with annual earnings exceeding US$100,000 accounts for the highest GMV share of 38.9% at amazon.com.

Amazon.com generally speaks to all age groups, but younger users are represented more than older ones. Amazon.com’s largest age group are online shoppers between the ages of 35 and 44 years, who generate 19.7% of GMV.

Shortly behind that follow users aged 45 to 54 years, confirming that more affluent users in their prime years, pun intended, account for highest GMV shares at amazon.com

Amazon’s digital-first approach clearly appeals to younger consumers, but it has broader implications as well. Amazon’s logic centers on reaching consumers from every angle, of which amazon.com is just the basic part. Loyal Amazon customers are sure to be Prime members, a subscription model which will be the least attractive to the youngest or oldest members.

That’s because Prime is designed to appeal most to shoppers with a steady income and frequent purchasing habits – groups that are more likely to be in the middle age brackets. Younger consumers may not see enough value in paying for the subscription, and older shoppers may not use the full range of benefits or may prefer the in-store experience.

Walmart.com's income pattern is in stark contrast to Amazon's customer segments.

Walmart is more obviously skewed toward older and lower-income consumer segments. In 2024, over 65-year-old consumers accounted for 21.2% of GMV on walmart.com. Every other segment generated a smaller share of GMV.

The same goes for income groups. 38.9% of walmart.com’s GMV is generated by customers in the lowest segment, defined as users earning less than US$60,000 annually.

Even though walmart.com has adopted some of amazon.com’s strategies in recent years, its consumer base skews towards older demographics. Force of habit surely plays a role, fueled by Walmart’s status as the number one hypermarket with bulk purchases and bargains around every corner.

The latter point also accounts for walmart.com’s appeal among lower-income segments, who value the combination of low prices and bulk package offers.

Although the two companies share certain similarities, maintaining competitiveness requires each to resonate with distinct customer segments. If their customer bases were too similar, their ability to differentiate themselves would weaken, leaving one player (most likely walmart.com) at a clear disadvantage. Recognizing and nurturing these distinctions ensures that both retailers can preserve their unique value in the market.

Related Articles

Electronics is not just consumer tech, as the top 100 retailers in the US market show. Here is who's behind the United States' largest category.

In the global top 10 ranking, Amazon holds the number one spot, yet it is still outnumbered. Players like Pinduoduo, Douyin, Taobao and Tmall follow close behind. Together with the others, they account for 80% of this top ranking.

Of the 30 fastest growing marketplaces, 17 have a third-party share of over 80%. This hints at a future of platform ecosystems over inventory-led business models.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.