What Are Future Trends in E-Commerce?

By 2030, e-commerce will be worth US$7 trillion. The trends driving this revenue are essentials over exciting categories, mobile-first omnichannel, and AI standing in for the search bar.

Market Concentration

The global number of mid-sized retailers is declining, and they are losing their grip on overall e-commerce revenues. Why market concentration endangers smaller businesses is the topic of this blogpost.

Nadine Koutsou-Wehling

Data Journalist

April 20, 2026

Market Trends, Retailers

Much of the conversation around e-commerce tends to focus on dominant giants or the rise of fast growing challenger brands. This framing misses a more consequential shift that is unfolding quietly beneath the surface. The middle tier of e-commerce is eroding.

We at ECDB frequently report on the rising concentration of the e-commerce market. But the increasing accumulation of revenues by top retailers on the one hand, has visible consequences on the smaller segment of businesses between US$10 million and US$1 billion of GMV on the other.

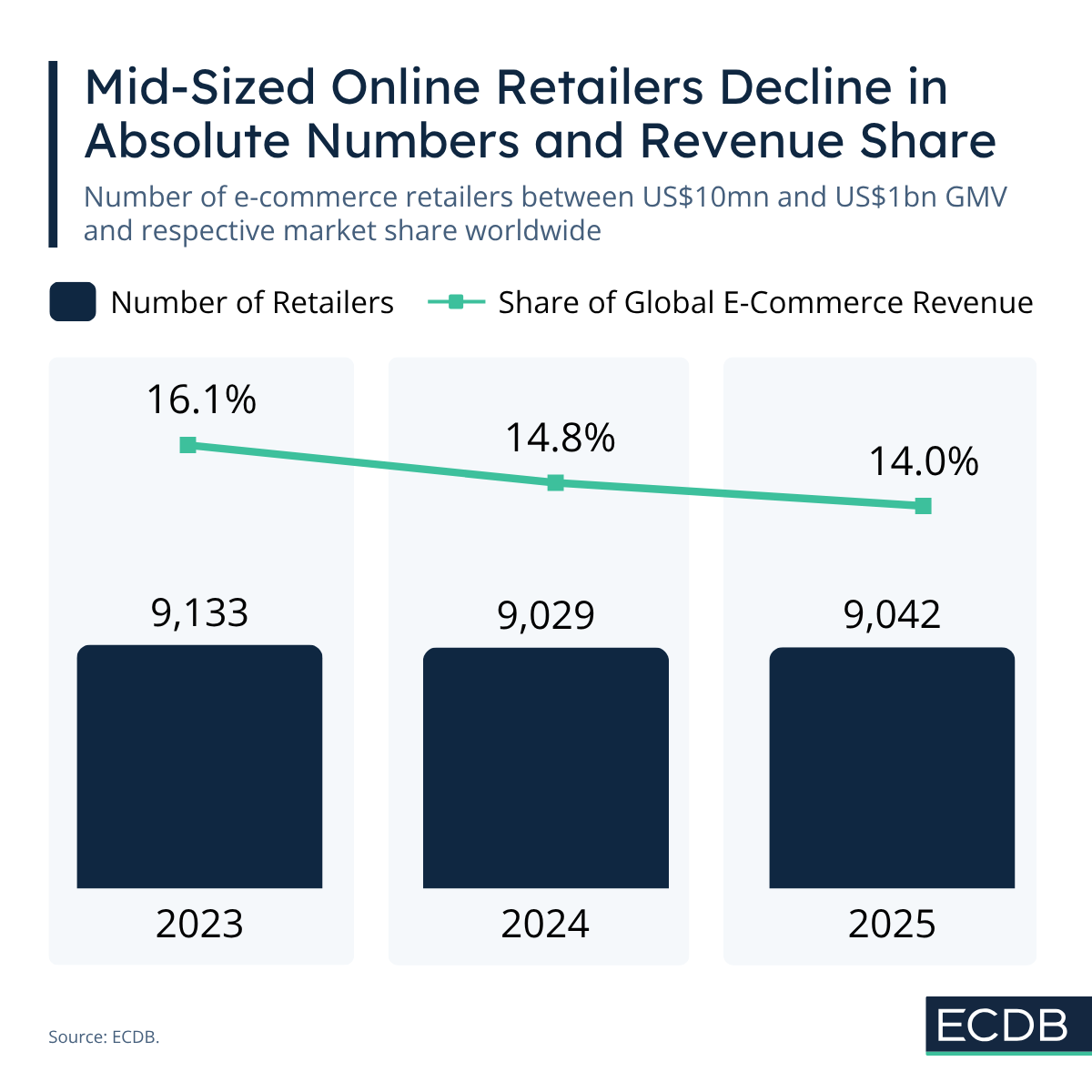

In 2023, there were 9,133 e-commerce retailers operating within this margin. Together, these companies accounted for 16.1% of global e-commerce revenues. The number of retailers declined in the next year and their share of revenues dropped to 14.8%. By 2025, the count showed only a marginal increase of 20 retailers, yet their share continued to fall, reaching 14.0%.

At the same time, the top end of the market is consolidating power. A small group of dominant e-commerce companies is capturing an increasingly disproportionate share of global revenues. This dynamic reinforces a winner takes most structure, where scale advantages compound over time.

What emerges is a hollowing out of the market. Companies in the smaller tier often lack the scale to compete with the largest platforms and the agility to differentiate like smaller niche players.

As our analysis of Amazon and its challenger retailers shows, smaller retailers attract fewer buyers, generate lower purchase frequency, and achieve the lowest spend per customer compared to rising brands. This gap in performance reflects the structural disadvantages that many mid-sized players face in a market that is increasingly determined by platform dominance and network effects.

The dynamic is ultimately self reinforcing. Leading marketplaces become unavoidable distribution channels for an increasing share of the market. Mid-sized and even emerging retailers find themselves with limited alternatives and are effectively compelled to sell through these ecosystems in order to remain visible and competitive.

The leading few therefore gather more commerce activity, data and customer relationship, which leads to a further tightening of the feedback loop that continues to erode the middle tier of e-commerce.

Related Articles

By 2030, e-commerce will be worth US$7 trillion. The trends driving this revenue are essentials over exciting categories, mobile-first omnichannel, and AI standing in for the search bar.

Central Europe consists of heterogeneous e-commerce markets, many of them at different stages of development. The expectation is that a fully autonomous agent will predict needs and carry out purchases with only minimal supervision. But the reality still looks different, depending on where one looks.

B2B e-commerce is being built by the same companies that already proved the model in B2C, and it's still barely digitized by comparison. Here's what that gap means for where it goes next.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.