Article in a Nutshell:

Retailer concentration: The top e-commerce platforms are growing faster than the rest of the market, with the top 5 capturing 56% of global GMV in 2025, up from 48% in 2022.

Emerging leaders: TikTok Shop (Douyin) and Pinduoduo saw significant gains, driven by data-driven engagement, low prices, gamification, and international expansion.

Asia's significance: Shopee and AliExpress entered the top 10, while eBay and Suning exited. 80% of the top positions are now held by Eastern companies.

Varying regional dominance: Amazon leads in Europe and the Americas, while Asia shows a more balanced but highly competitive market with multiple platforms generating hundreds of billions in GMV.

Global e-commerce is increasingly dominated by a handful of players. The top platforms continue to grow at a faster rate than the rest of the market. This market dynamic is driven by economies of scale, network effects, and customer loyalty, as well as the technological advantages of leading players.

AI-driven personalization, advanced logistics, and seamless omnichannel integrations make these leaders stand out from the rest and amass increasing shares of the global market.

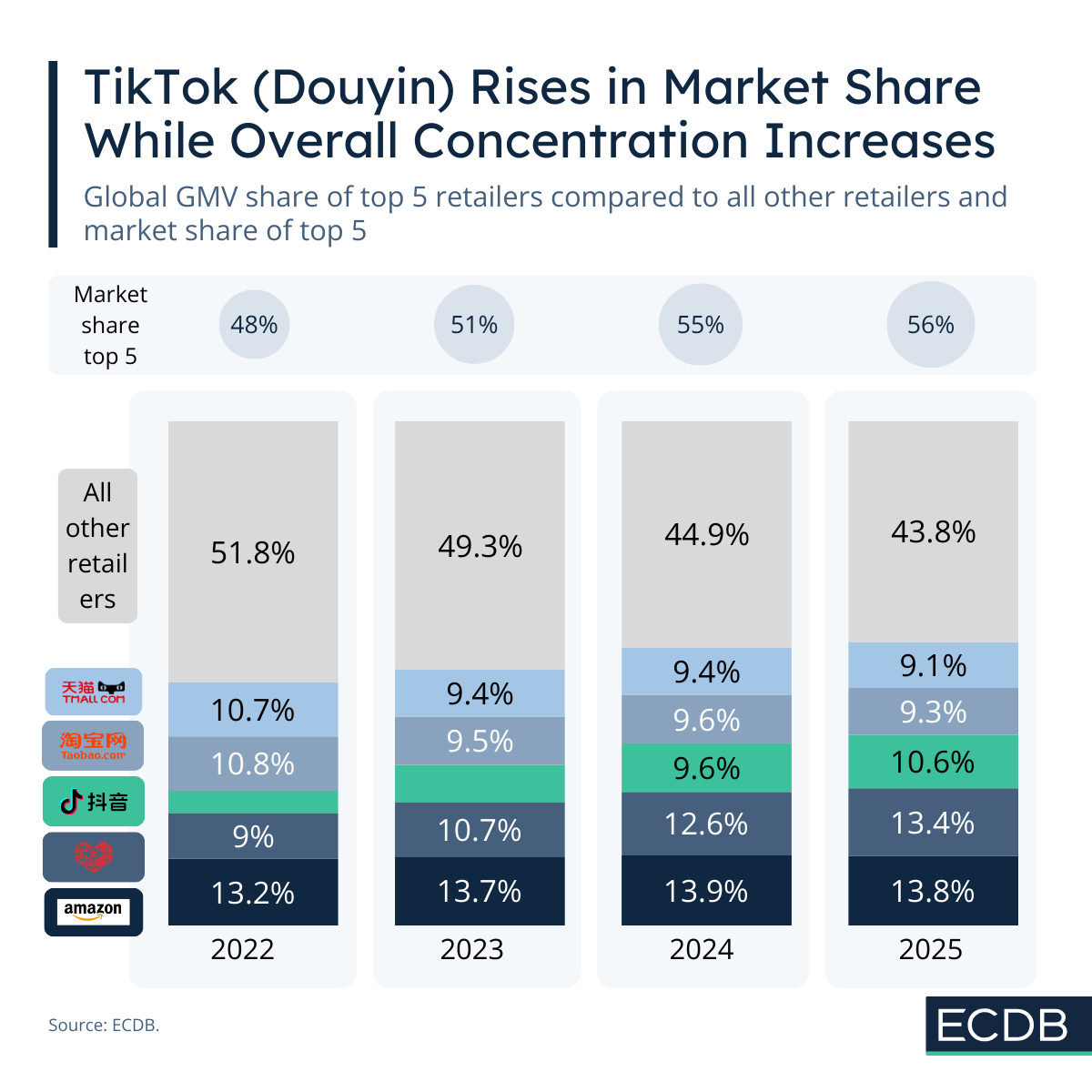

The Top 5 E-Commerce Retailers Capture 56% of the Global Market

In 2025, the top 5 e-commerce retailers collectively held a market share of 56%, up from 48% in 2022. This demonstrates accelerating market concentration, as the largest platforms pull further ahead of smaller competitors.

One of the clear winners in the recent years was TikTok Shop (Douyin), which increased its market share from just 4.5% in 2022 to 10.6% by 2025. Similarly, Pinduoduo expanded significantly from 9.0% market share in 2022 to 13.4%% in 2025.

Both platforms use a data-driven approach to engage users and incentivize shopping. Low prices, gamification, and internationalization are core drivers of their strategy and have proven successful over the years.

Amazon, other than Tmall and Taobao, cemented its position and expanded its market share despite its maturity. Even in a competitive e-commerce environment with challenging market realities, Amazon grew its market share from 13.2% to 13.8%. Its example shows how even established incumbents can grow past their mature stages.

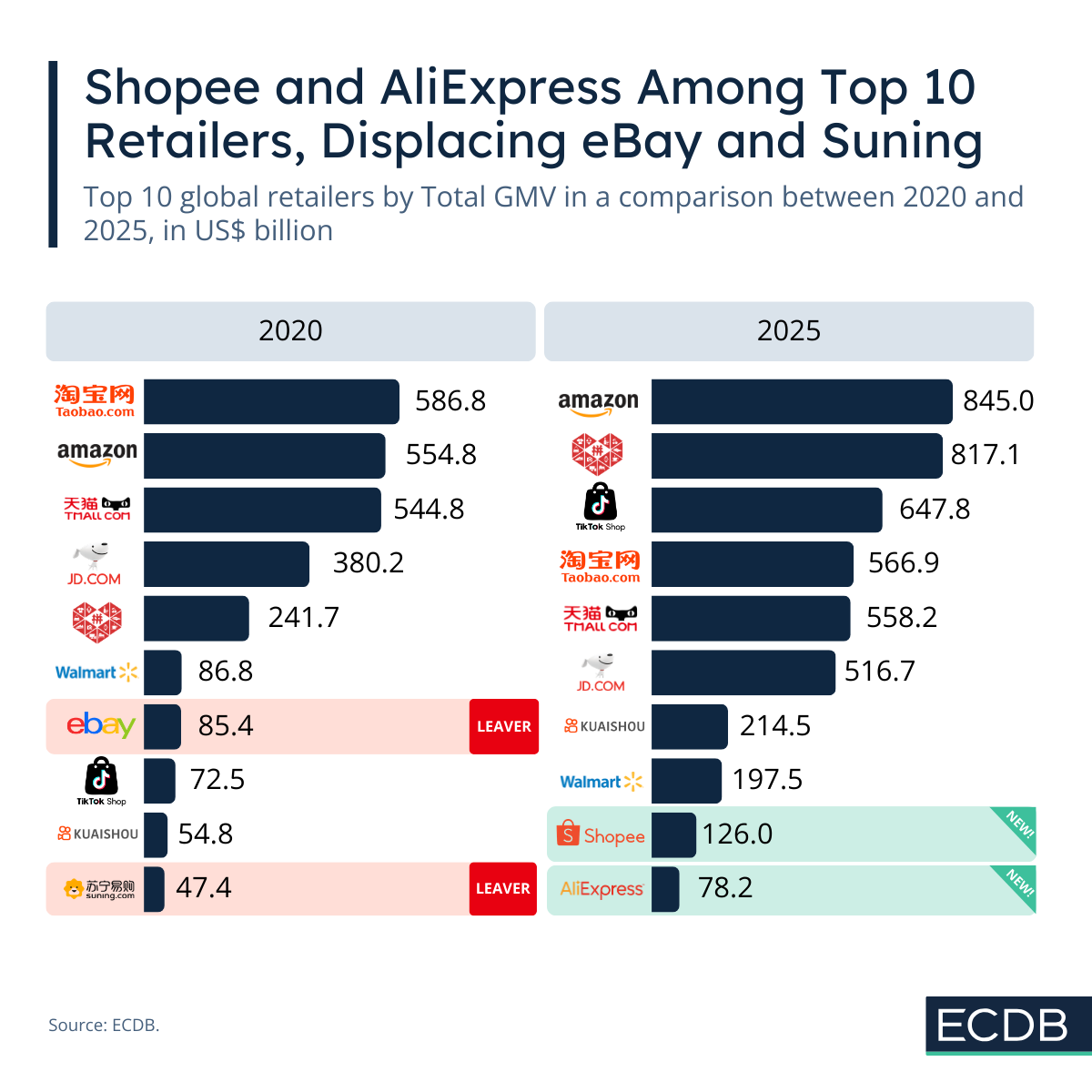

Shopee and AliExpress Rose to the Global Top 10 Online Retailers

Since 2020, the top 10 e-commerce retailers have not changed fundamentally. Instead, the top 10 have increased their dominance, with only minor shifts occurring at the lower end of the ranking. Amazon became number one since 2020, growing its GMV from US$586.8 billion in 2020 to US$845.0 billion by 2025.

Most notably, eBay and Suning exited the top 10 while Shopee and AliExpress joined. The changes underline an Asian prevalence in the top 10 e-commerce retailer ranking, where 80% of positions are held by platforms from the East.

A closer look at regional rankings reveals different varieties of market concentration.

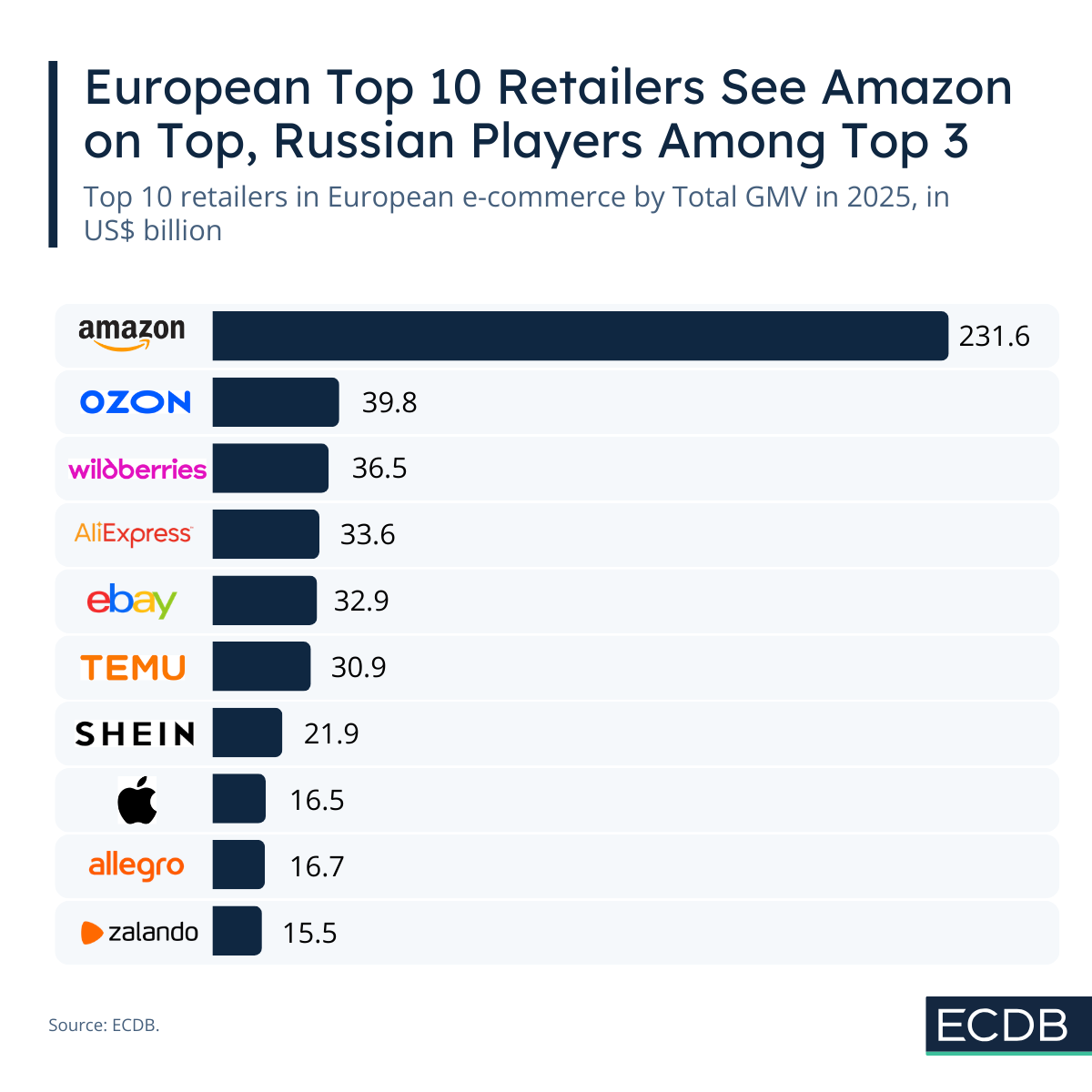

Europe: Amazon Towers Over Remaining Players

Even though Europe is a diverse market with a wide spectrum of national conditions and consumer preferences, its e-commerce winner is clear: Amazon holds the top position with a GMV of US$231.6 billion.

Amazon's leadership is followed by Russian marketplaces Ozon and Wildberries, as well as Asian contenders AliExpress, Temu, and Shein. The only homegrown European players in the top 10 are Allegro and Zalando, occupying the ninth and tenth spots respectively.

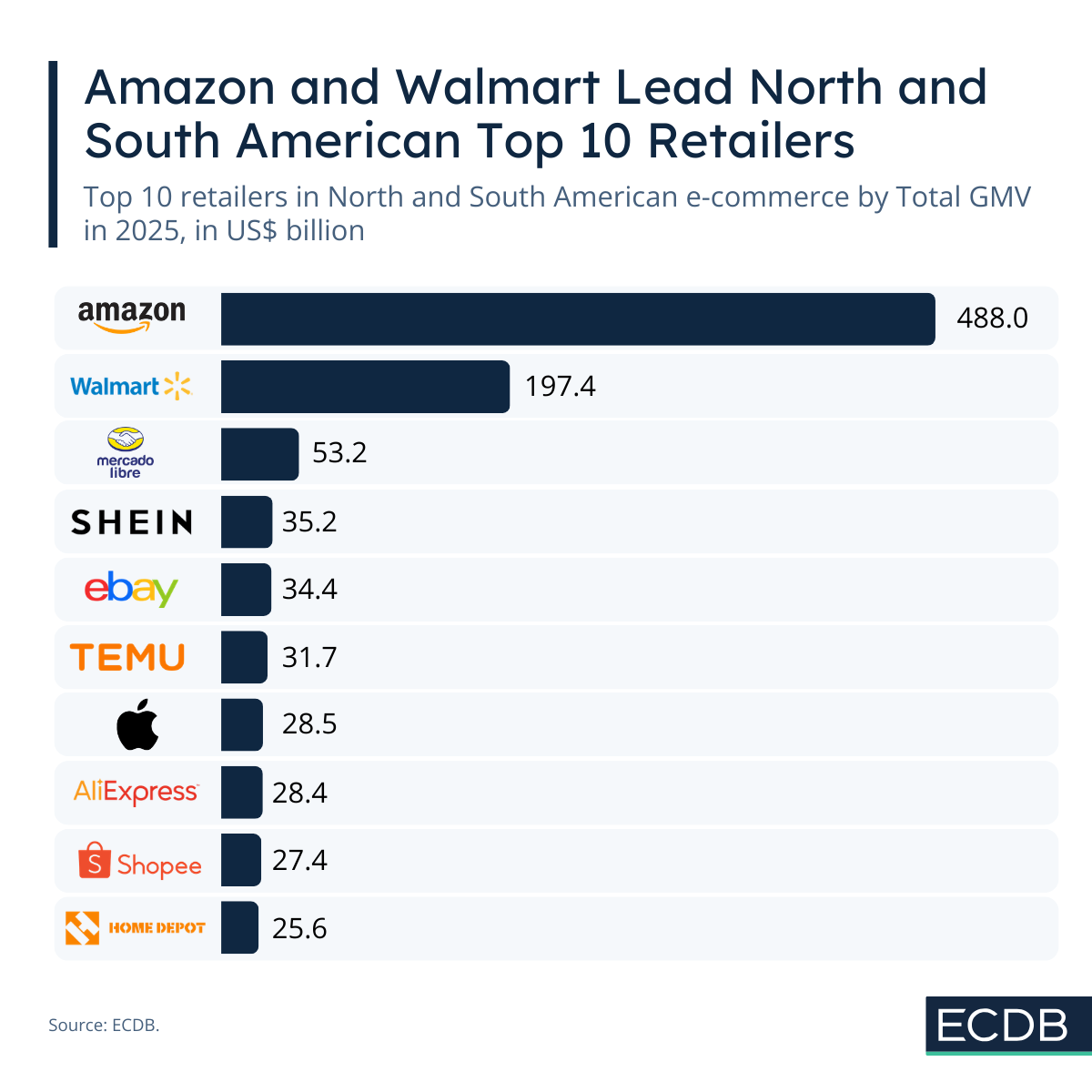

Americas: Amazon and Walmart Dominate the Market

In the Americas, Amazon’s GMV reaches US$488.0 billion, followed by Walmart at US$197.4 billion. Despite the rapid rise of rivals Mercado Libre and Shopee, they remain far behind the two market leaders.

Other notable risers include Shein (US$35.2 billion), Temu (US$31.7 billion), and AliExpress (US$28.4 billion), each of them among the most hotly discussed platforms in online retail in recent years. Their fast-fashion strategies, combined with wide cross-border reach and price competitiveness, have sparked debates over tariffs and protectionism.

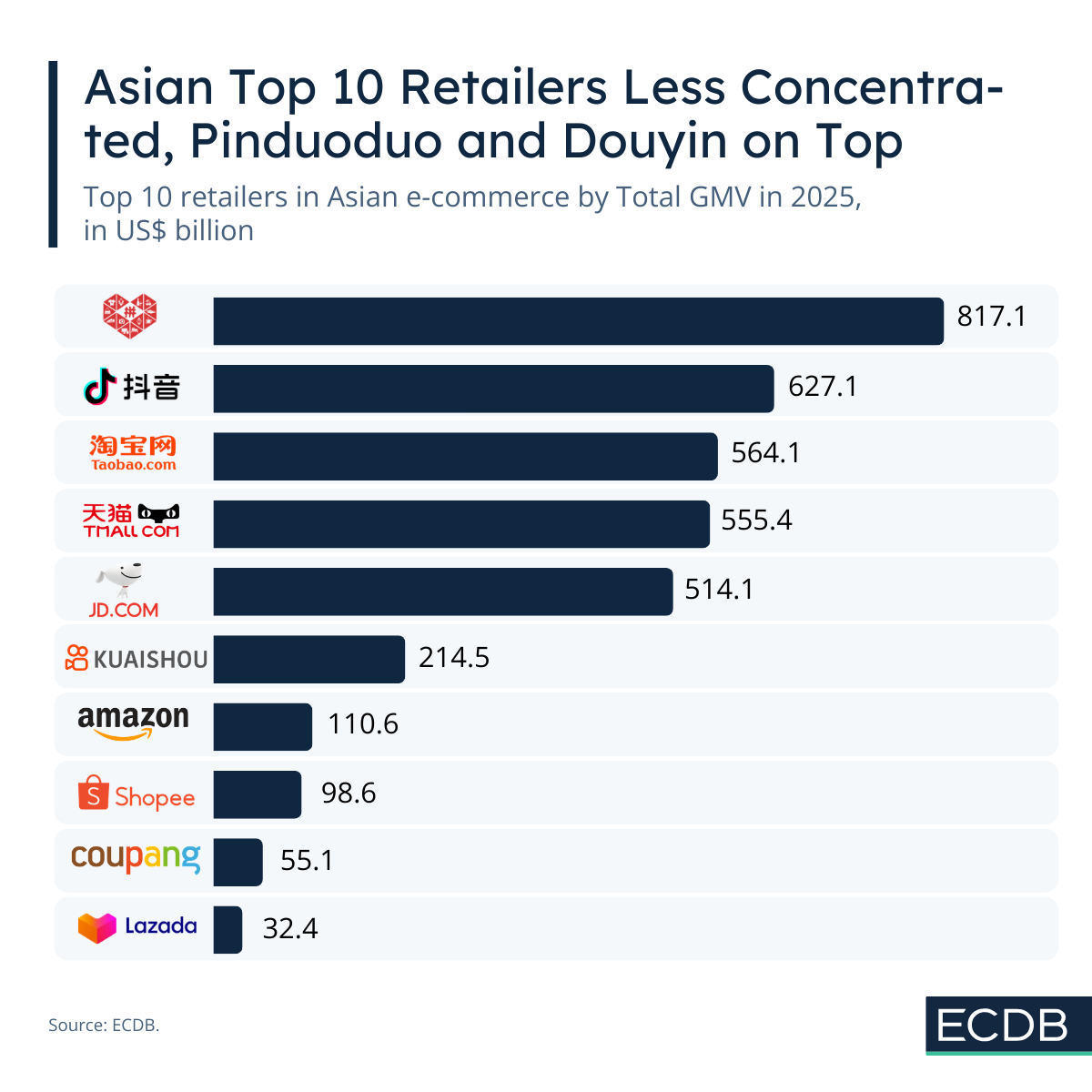

Asia: E-Commerce More Balanced Across Multiple Players

The Asian top 10 ranking looks much different from previous years. In China and Southeast Asia, multiple platforms generate hundreds of billions in GMV. They create a more balanced, yet intensely competitive, market.

Key examples include:

Pinduoduo, sister company of Temu, with a GMV of US$817.1 billion almost as high as Amazon's global GMV.

Douyin (TikTok Shop) generated a GMV of US$627.1 billion.

Taobao and Tmall both with around US$560.0 billion in GMV.

JD.com, which generated US$514.1 billion in 2025.

A few more giants dominate Asia’s e-commerce, but it remains highly concentrated, showing how government regulation and rapid digital acceleration can produce world-class e-commerce platforms within just a few decades.

Retailer Concentration in E-Commerce

E-Commerce is concentrated among the hands of a few powerful, tech-driven platforms. While Amazon continues to dominate in the West, Asian players like Pinduoduo, Douyin, Shopee, and AliExpress are reshaping the top rankings with massive GMV, innovative engagement strategies, and international expansion. Social commerce, gamification, and data-driven personalization are proving decisive. As market concentration rises and consumer behavior evolves, the platforms that combine scale, technological sophistication, and cross-border reach will define the future of global online retail.