June 2026 E-Commerce Recap: US$436.8 Billion in Global Revenue

The start of summer brought positive developments in June, with US$436.8 billion in global e-commerce revenues and a 9.5% year-on-year increase. Read on for the details here.

3P Marketplace Dominance

The marketplace trend is in full swing. Globally, third-party marketplaces are gaining ground. But which region dominates? Find it out here.

Nadine Koutsou-Wehling

Data Journalist

April 13, 2026

Market Trends

Article in a Nutshell

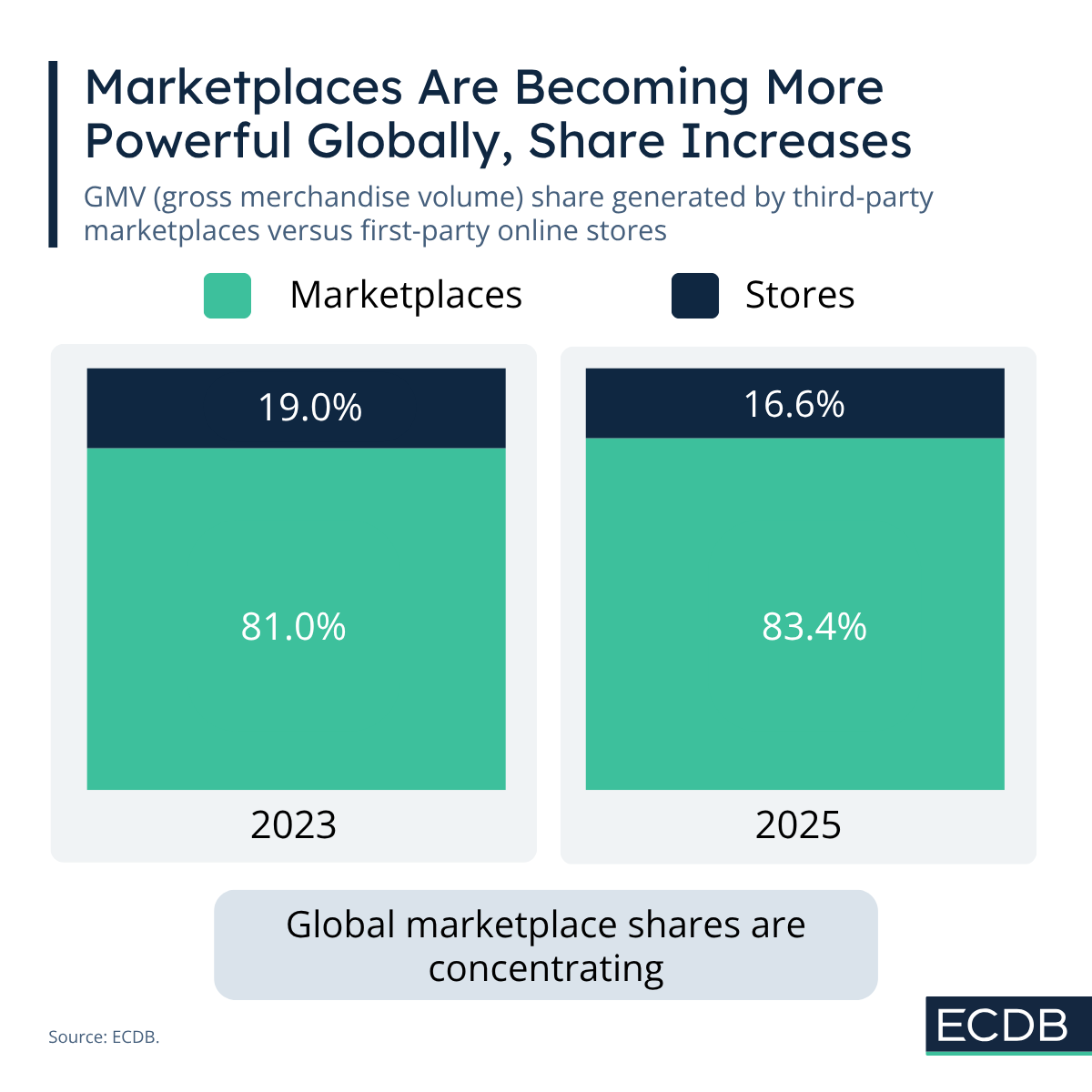

Globally, marketplaces now generate 83.4% of e-commerce GMV, while first-party online stores account for just 16.6% in 2025.

Third-party marketplace adoption is growing in every region, though benchmarks vary significantly by location.

Europe sees moderate marketplace penetration at 60.8%, the Americas show mixed adoption, and Asia leads with 97% of e-commerce revenue flowing through marketplaces.

The trend toward third-party marketplaces is expected to continue, driving further concentration of top platforms worldwide.

E-commerce is no longer just about running your own online store. Around the world, marketplaces are taking a central role in shaping how consumers shop. In fact, 83.4% of global gross merchandise value (GMV) is now generated through marketplaces. But depending on which region you are operating in, the benchmark differs.

It is clear that marketplaces are becoming more prevalent globally, which is also why the share of global e-commerce revenues generated through third-party (3P) marketplaces grows. 3P means that revenues are generated through external sellers on a platform, in contrast to first-party (1P), which denotes revenues made from brand owners directly.

In 2023, 19.0% of global e-commerce revenues were made by 1P online stores. This share has shrunk to 16.6% by 2025. In turn, 3P revenues generated on global marketplaces grew from 81.0% to 83.4%. There is one region in particular that corresponds to this majority, even though 3P shares are increasing everywhere.

In Europe, where many heritage brands traditionally focus on direct-to-consumer sales or their own online stores, the share of GMV from third-party marketplaces is lower than in Asia. In 2025, 60.8% of European e-commerce revenue comes from marketplaces, up from 56.2% in 2023.

In the Americas, the picture is mixed. North American brands still rely heavily on their own online stores, while South American consumers favor large marketplaces such as MercadoLibre and Shopee. In many of the emerging markets, most GMV flows through these ecosystems.

Asia stands apart with marketplace dominance. Since 2023, the marketplace share of Asian e-commerce revenues expanded even more to reach 97.0% in 2025. This is because major platforms played a central role in building e-commerce infrastructure in the region. Marketplaces created habits that continue to influence online shopping today.

Marketplaces are becoming more influential everywhere but nowhere do they dominate as much as in Asia. Third-party platforms helped build e-commerce ecosystems in the region and are therefore now omnipresent. But the trend towards 3P-marketplaces is also visible in the Americas and Europe, where shares range between 60.0% and 70.0% in 2025. In the coming years, this trend is expected to lead to further concentration of top marketplaces.

Related Articles

The start of summer brought positive developments in June, with US$436.8 billion in global e-commerce revenues and a 9.5% year-on-year increase. Read on for the details here.

Central Europe is dominated by one market in particular: Germany. The others follow at a far distance. They include Poland, Austria, Switzerland, and Greece. Here is how they compare.

In Italy, 66% of the top 250 online store's net sales are generated by the top 5. This makes it the most concentrated market among the EU-Big Five. What does that mean for e-commerce? Find it out here.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.