Where Does Cross-Selling E-Commerce Convert Best and Why?

Cross-selling is one of those e-commerce strategies used to improve e-commerce sales. But for whom does it make sense? Which other strategies are aligned with it?

Product Categories With Real Demand

A successful e-commerce product launch strategy doesn't rely on size alone. Transaction data shows where the market is currently still open.

Nadine Koutsou-Wehling

Data Journalist

July 10, 2026

Transactions

Article in a Nutshell:

Growth trajectory beats market size as an entry signal: Household Care is accelerating faster than any other tracked category despite ranking just 19th by revenue.

AOV determines the business model before launch: Household Care runs on US$40.30 and repeat purchases, Bullion & Precious Metal runs on US$574.44 and trust.

Fragmentation reveals real whitespace: Household Care spans 2,357 stores with no vertical specialist in the top ranks.

Global e-commerce revenue is on track to hit US$5.36 trillion in 2026, but that growth is not evenly distributed. The categories that look most attractive on the surface are often the ones already locked down by a handful of dominant players, while quieter categories are compounding growth underneath the radar.

Real demand shows up in the transaction data before it shows up in a trend report: in accelerating growth, in category economics, and in how concentrated or fragmented the competitive field already is.

The following framework, built on three contrasting categories, shows how to tell the difference before committing capital to a launch.

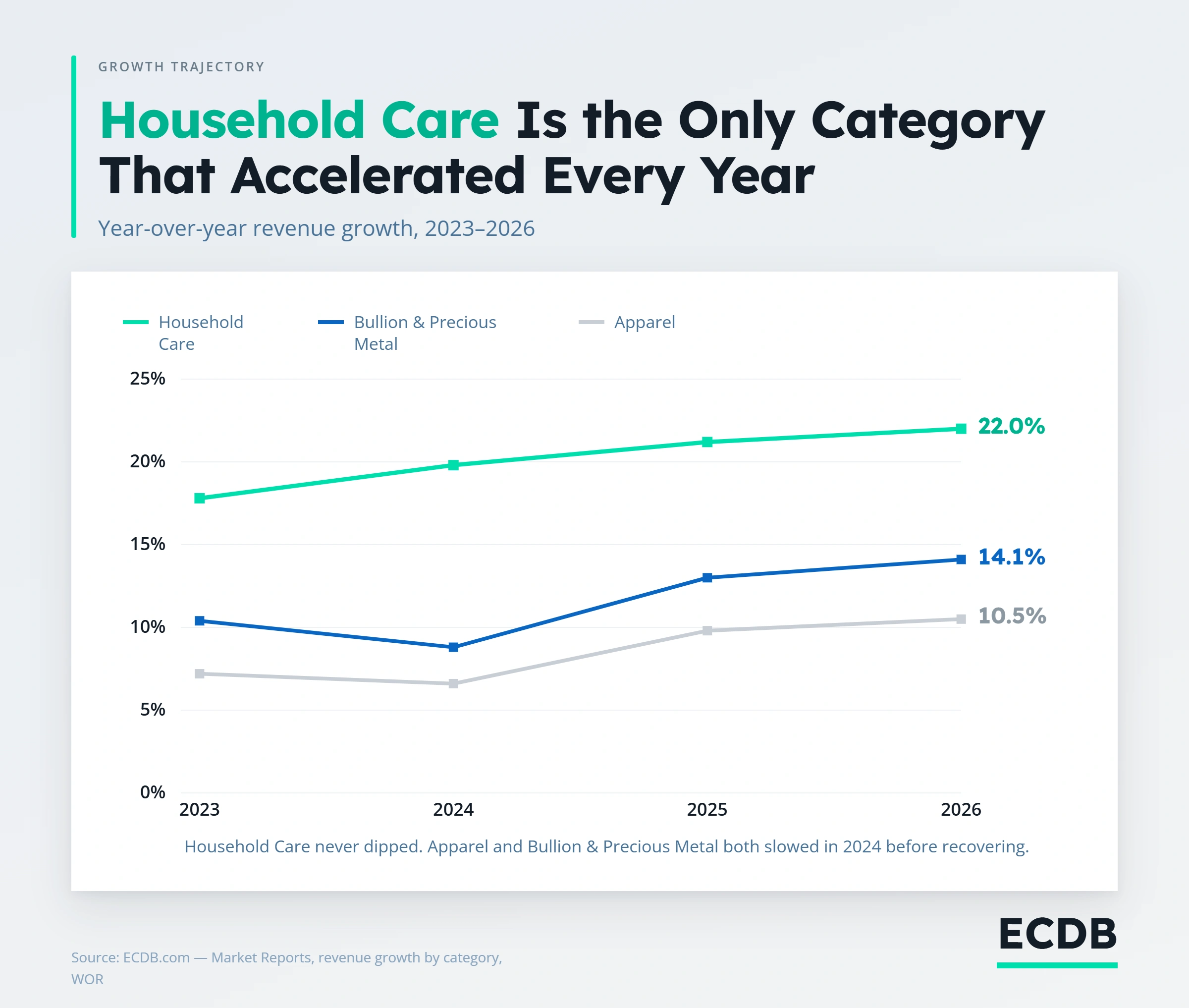

A category worth entering is one where demand is still building, not one that is simply large. Household Care illustrates this clearly: global revenue growth for the category has accelerated every year since 2023, from 17.62% to 19.71% to 21.18%, with 22.03% projected for 2026, making it the fastest-growing category ECDB tracks globally.

That acceleration is happening in a category worth US$70.8 billion in 2026, which is a real, investable market, just not the biggest one on the board.

Apparel tells the opposite story. It is the largest category tracked, worth US$767.2 billion in 2026, and growth has ticked back up to 10.49% after dipping to 6.6% in 2024. But a market that size, growing at that rate, is a mature market defended by entrenched players rather than an open field.

Size signals that a category is relevant. Growth trajectory shows that there is still room to grow in it.

Bullion & Precious Metal sits in between and makes the case for looking at multiple years rather than one. It cooled down from 10.30% in 2023 to 8.8% in 2024, is then projected to pickup growth again, reaching 14.1% in 2026. A single look at the cooldown in 2024 would not have been sufficient.

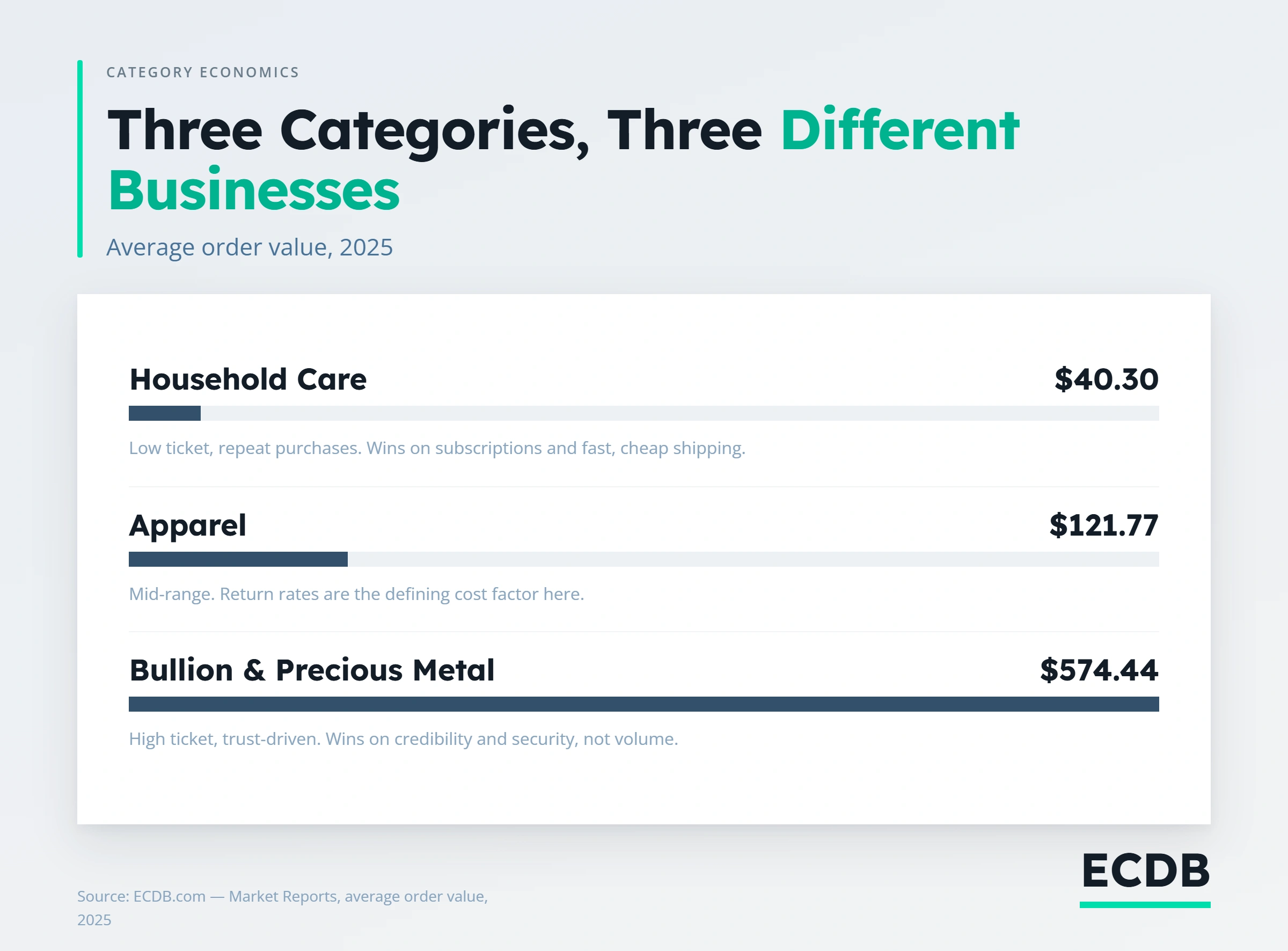

Average order value (AOV) determines whether a category rewards volume or margin, and that decision shapes logistics, marketing, and cash flow long before launch.

The three categories examined here sit at three different points on that spectrum:

Household Care: US$40.30 AOV. That is a low price point, which means the category runs on repeat purchases rather than one big sale. A brand entering this space needs to think about subscriptions, restocking reminders, and fast, cheap shipping, because customers are meant to come back often.

Apparel: US$121.77 AOV. Mid-range, with return rates as a defining economic factor that categories at the extremes do not deal with in the same way.

Bullion & Precious Metal: $574.44 AOV. Customers there make fewer, bigger purchases and need to trust the seller before they buy. This calls for a different approach than in Household Care: credibility, security, and clear information, rather than volume and repeat orders.

None of these AOV profiles is better than another. They are different games, and the mistake brands make is applying a volume playbook to a trust-driven category, or a trust-driven sales approach to a category that needs to win on frequency and repeat purchase.

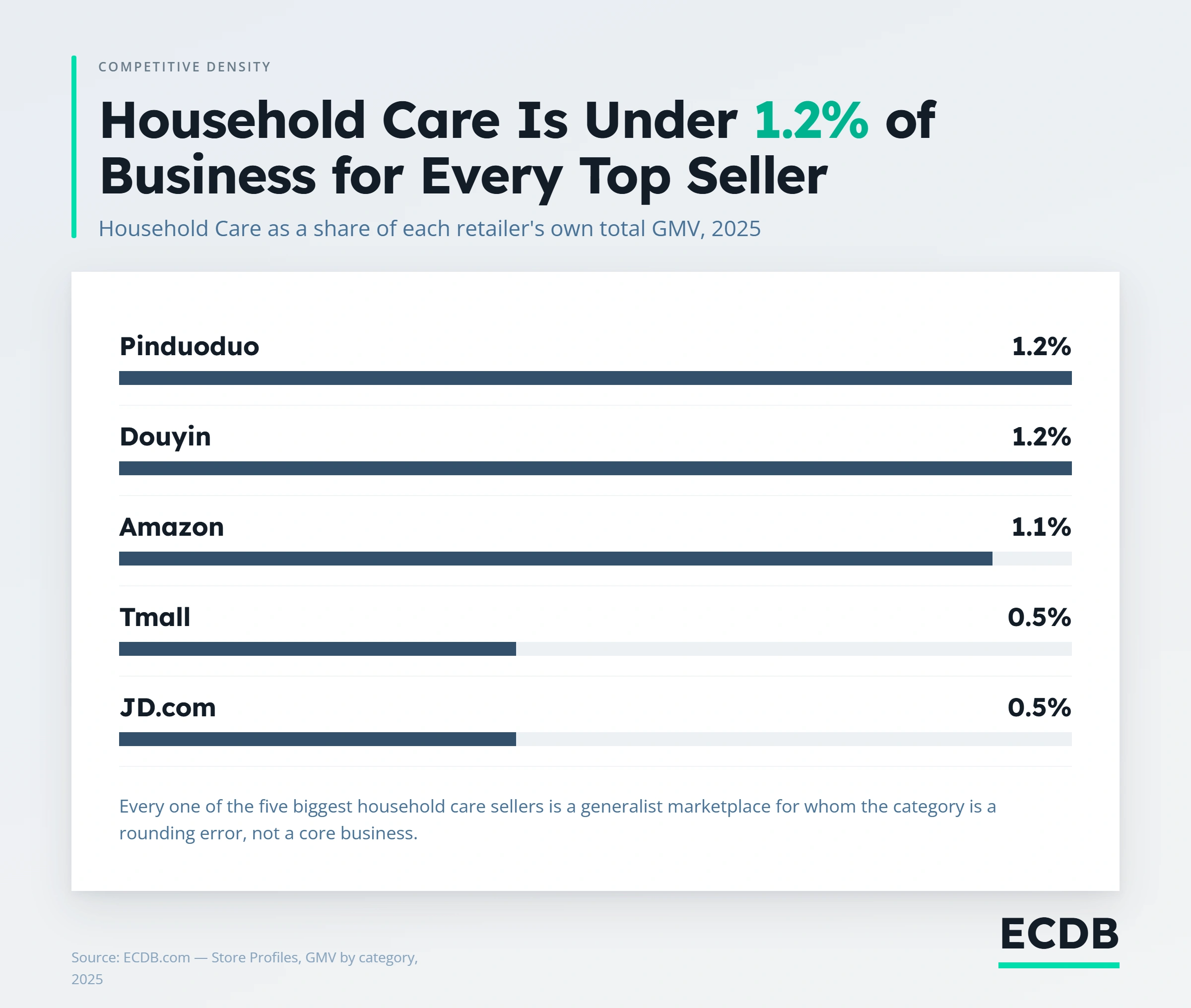

Before assuming a category is open, check who already occupies the top of the ranking. Household Care has 2,357 stores tracked globally, and its top ten by GMV are broad marketplaces such as:

None of them is a household care specialist. That leaves an opening for a focused brand to win on a smaller, better-curated range or better service, rather than fighting a category leader that has already built a dedicated audience.

This is the check that matters most before calling a category "underserved." A fast-growing category with no dominant specialist is a real opportunity. A fast-growing category already ruled by two or three focused competitors is a much harder fight, even if both look identical in a simple growth chart.

The case gets stronger once these five stores' own numbers are checked. Household Care makes up just 1.2% of Pinduoduo's total GMV, 1.2% of Douyin's, 1.1% of Amazon's, and only 0.5% of both Tmall's and JD.com's. Every single one of the five biggest sellers of household care products treats it as a rounding error in their own business, not a category they're building around.

That is a different, harder kind of evidence than simply noting that these are general marketplaces. It confirms that none of them has a reason to defend the category the way a specialist would defend its core business.

A brand entering household care is facing generalists for whom losing this category wouldn't move their own numbers at all.

The same method used to find Household Care works for any category: A category is worth entering when it passes all three checks, not just the one that happens to look best on its own.

Right now, Household Care passes all three. The next category to watch will be the one that starts showing the same pattern.

Every figure used to build this case, growth by year, AOV, and who already sells in a category, comes from data ECDB tracks across over 18,000 categories and thousands of stores. That's what turns a category decision from a guess into something testable: instead of assuming a market is open because it feels underserved, a brand can run the same three checks used here on any category on its shortlist.

That's the practical use for a brand deciding where to expand next. Run growth trajectory, AOV, and competitor density on a few candidate categories before picking one, the same way this article picked Household Care over Apparel and Bullion & Precious Metal. The category that clears all three checks, not just the one with the best headline growth number, is the one worth expanding into.

Brands that want to run this check on their own shortlist can pull the same growth, AOV, and ranking data through ECDB's Category Explorer and Rankings tools.

Related Articles

Cross-selling is one of those e-commerce strategies used to improve e-commerce sales. But for whom does it make sense? Which other strategies are aligned with it?

New data shows that for specialist marketplaces, adding adjacent categories is the more sustainable path to revenue growth than acquiring new buyers. Two case studies, Zalando and Trendyol, show how it's done.

Free returns feel like a basic expectation in e-commerce, but new data shows they are far more than a convenience feature. A consumer survey in Germany shows that return fees significantly influence how shoppers buy their online products.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.