Younger Consumers Drive Low-Cost E-Commerce Growth: Temu, TikTok and Shein

Temu, TikTok and Shein are known for their low cost and high product variety: Here is proof that they are primarily used by younger shoppers. But exceptions remain.

China Leads Singles Day

Singles Day 2025 remains the world’s biggest eCommerce event — but mostly in name. While the date 11.11 (Single Day 11.11) gains recognition outside Asia, real participation is still centered in China, where Alibaba, JD.com, and Pinduoduo dominate sales and where live commerce continues to reshape digital retail. Globally, awareness exists — but engagement remains limited.

David Niemeier

November 12, 2025

Other

Article In A Nutshell:

Singles Day 2025 remains the world’s largest shopping event, but its reach is still limited outside Asia. Globally, 61% plan to join a major sales event, yet only 33% know Singles Day. In Germany, awareness drops to 21%, and just 17% plan to shop, far from China’s scale. There, the event continues to expand: GMV rises to 1.56 trillion RMB, though daily sales fall as campaigns stretch to 27 days. Alibaba holds 55% of total GMV, JD.com 29%, while top categories such as Household Appliances, Phones, and Clothing make up around 37% of sales. Meanwhile, live commerce contributes a quarter of total GMV, turning Singles Day into a long, interactive retail season that still belongs firmly to China.

While 61% of consumers globally plan to join at least one major sales event in 2025, only 33% know about Singles Day. In Germany, awareness is even lower — 21% know it, and only 17% plan to shop. This shows that Singles Day remains a mostly regional event: globally recognized, but rarely acted upon outside Asia.

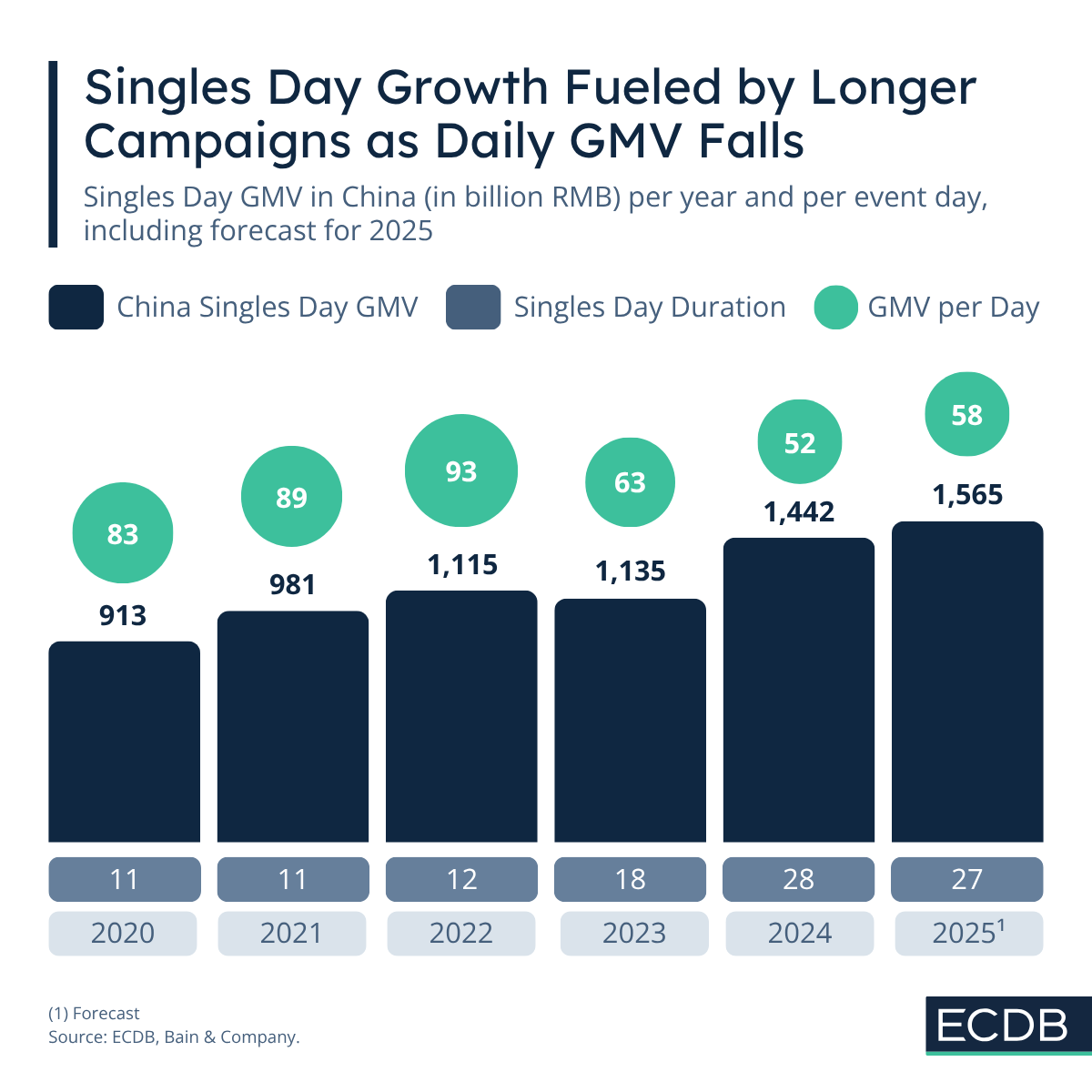

In China, the story is different. Singles Day 2025 continues to grow in total volume — from 913 billion RMB in 2020 to a forecasted 1.56 trillion RMB in 2025. But average daily GMV is declining — from 83 to 58 billion RMB — as retailers extend the event from a single day to a 27-day campaign. Singles Day has become a multi-week sales season, reducing pressure on logistics while maintaining customer engagement through constant deals.

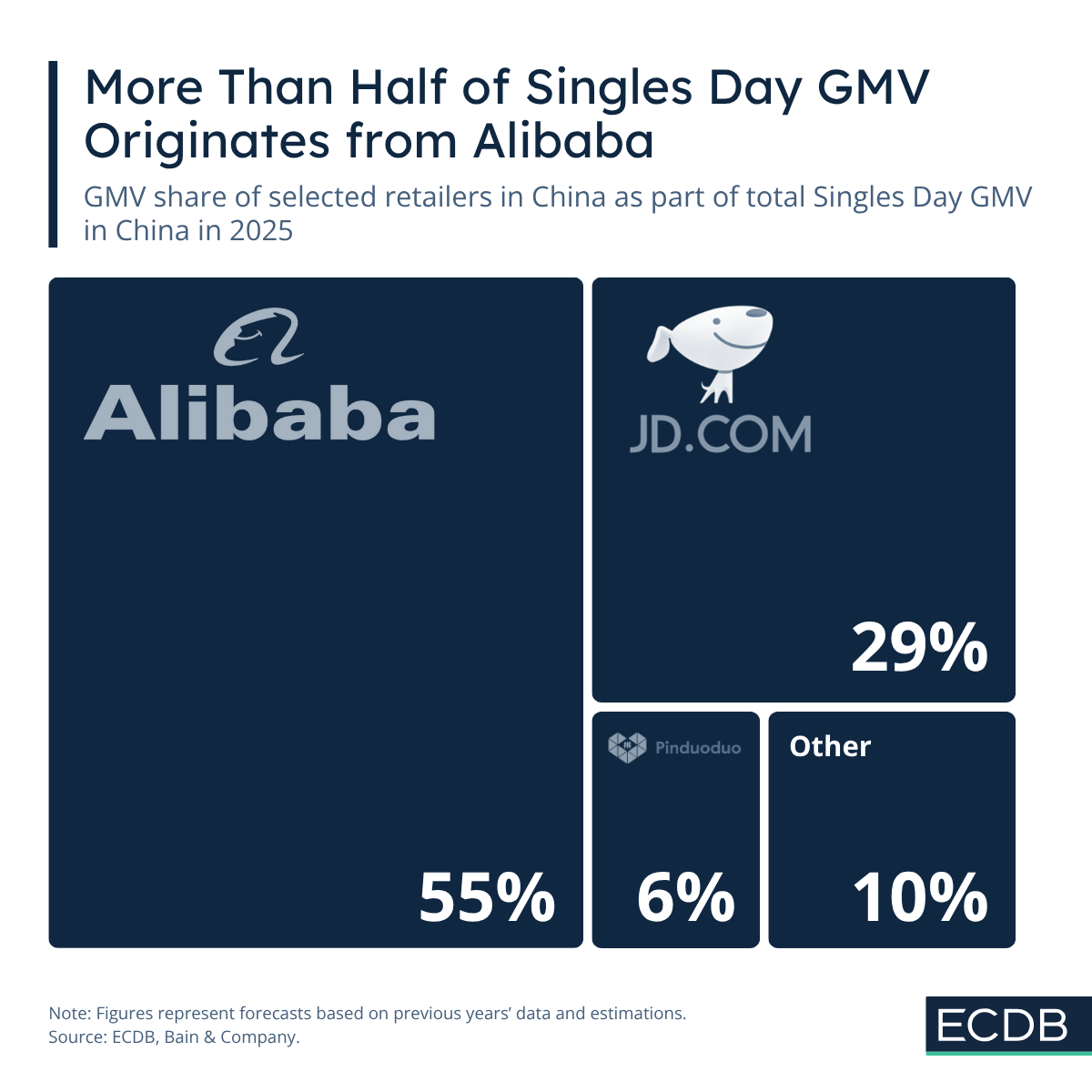

Alibaba accounts for 55% of Singles Day GMV, followed by JD.com (29%) and Pinduoduo (6%), leaving just 10% for all others. These three giants control over four-fifths of total GMV. Western brands like Zara (Zara Singles Day deals) or Amazon (Single Day Amazon offers) occasionally join the event, but their contribution remains marginal.

Singles Day 11.11 continues to be a uniquely Chinese eCommerce ecosystem.

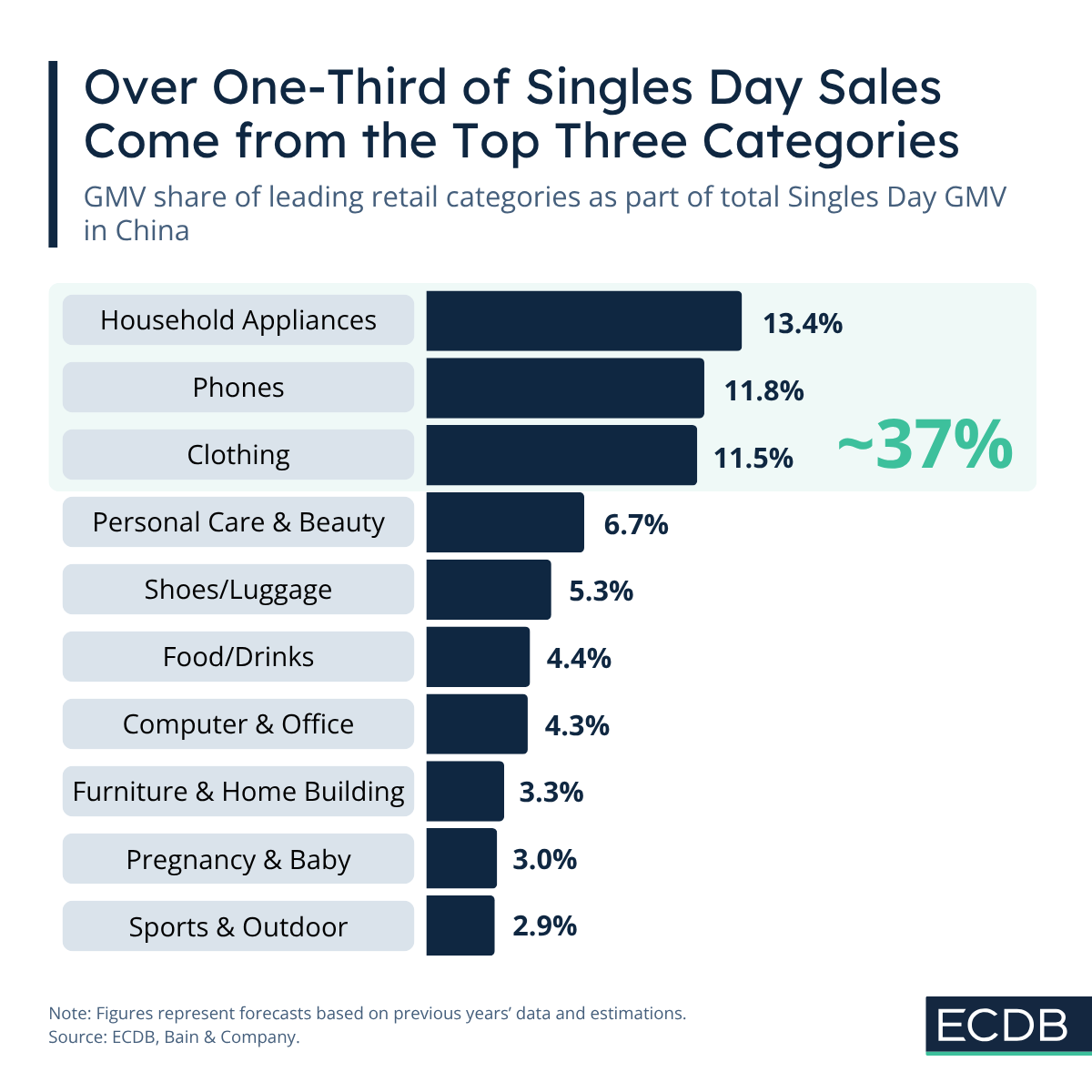

The top-performing categories — Household Appliances (13.4%), Phones (11.8%), and Clothing (11.5%) — together account for around 37% of total GMV.

These are precisely the kinds of products where discounts and visibility matter most, confirming that single day shopping remains driven by price-sensitive, high-value segments.

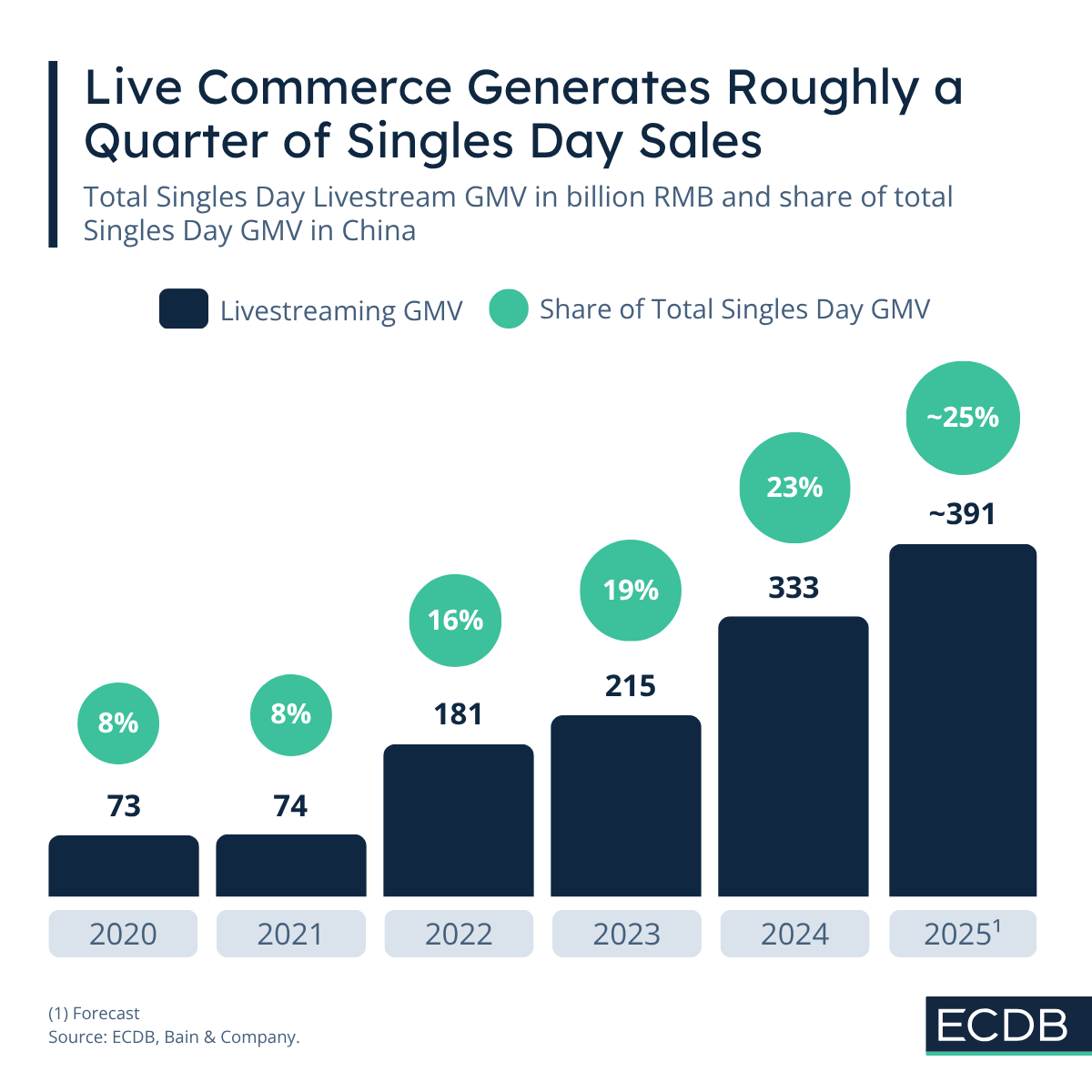

By 2025, live commerce is expected to generate 391 billion RMB, roughly 25% of all Singles Day GMV. The rise of livestreaming — where influencers, brands, and platforms merge entertainment with shopping — continues to make Singles Day the benchmark for interactive digital retail.

Singles Day 2025 underlines a sharp contrast: High awareness in China, low engagement elsewhere. While global recognition is growing slowly, Singles Day remains a phenomenon rooted in Chinese retail dynamics — driven by platform dominance, category focus, and the rise of live commerce.

For Western retailers, the lesson is strategic: Joining Singles Day could mean acting as a first mover, using early November to test campaigns or capture attention before Black Friday. But without clear consumer demand or brand fit, it risks becoming a costly distraction rather than a meaningful opportunity.

In short — the world watches, China sells.

Related Articles

Temu, TikTok and Shein are known for their low cost and high product variety: Here is proof that they are primarily used by younger shoppers. But exceptions remain.

Agentic commerce is a new way of shopping that affects retail platforms and sellers alike and is poised to become the dominant source in product discovery and purchase decisions.

Competitor analysis is an essential part of every business journey. Here's how to use the Analyze & Compare Feature at ECDB to make the most of the extensive data available.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.