The UK fashion e-commerce market is undergoing a major reshuffle. New digital-first disruptors are overtaking many of the country’s traditional fashion giants.

Platforms like Temu, Shein, Vinted, and TikTok Shop are reshaping consumer behavior with their low prices, wide selection, and strong social commerce integration.

Only a few UK fashion players manage to maintain a cutting edge in the dynamic sector that is fashion – they are discussed in the following.

Four Digital-First Players Who Change UK Fashion: Temu, Shein, Vinted, TikTok

Temu and Shein are not entirely responsible for the recent market shifts, even though they belong to a wave of new platforms that displace other brands from their former ranking positions.

Together with TikTok Shop and Vinted, these four players are the global disrupters of fashion e-commerce. TikTok Shop’s sister company, Douyin, is already on its way to the top of global apparel rankings.

The United Kingdom was the European e-commerce market where TikTok Shop debuted. By now it is available in six European markets. Similar to the other platforms in this focus (Temu, Shein and Vinted), price and product variety are the deciding factors for consumers.

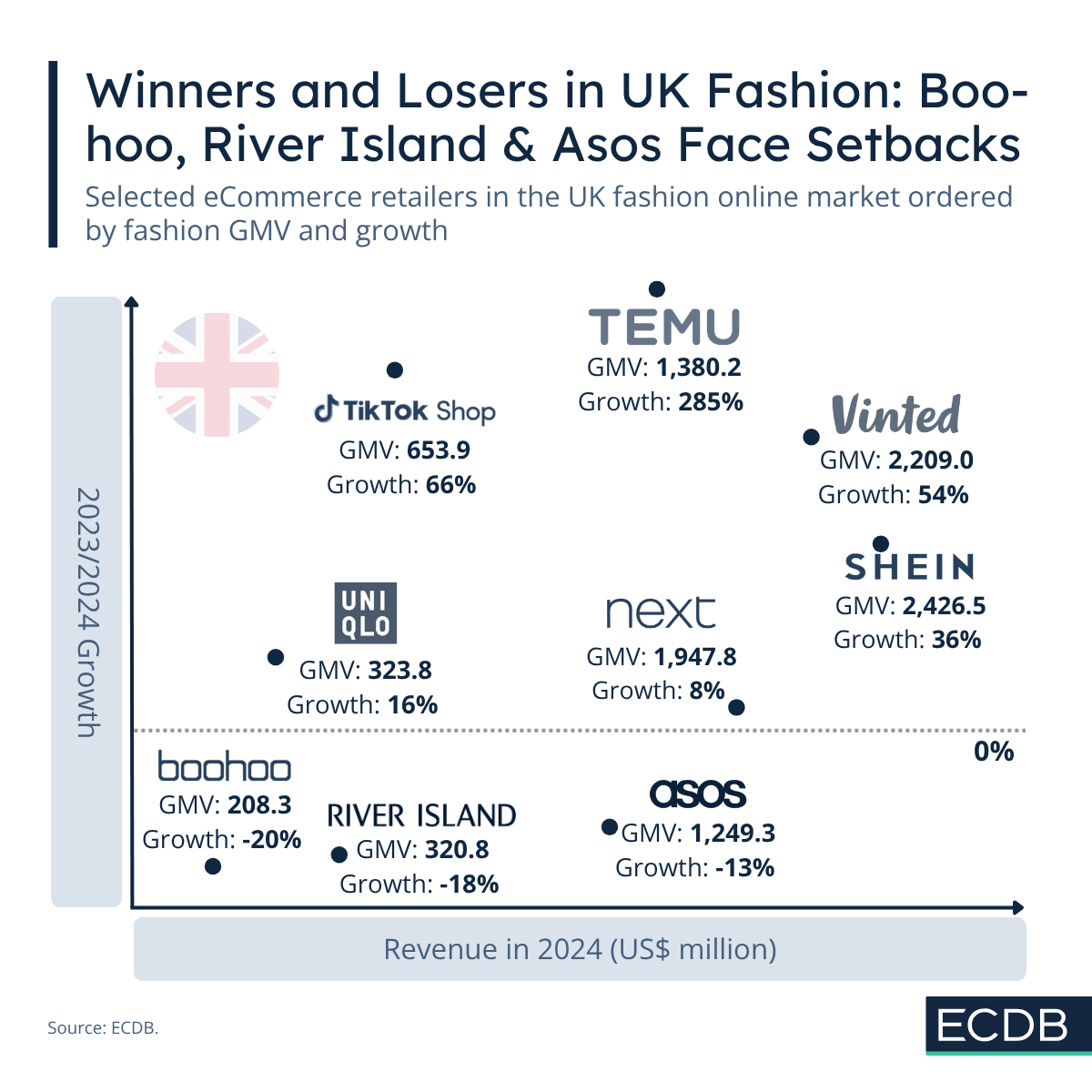

Of the four, Vinted and Shein generated the highest fashion GMV in the UK, with US$2.2 billion for Vinted and US$2.4 billion for Shein. But Vinted's growth rate from 2023 to 2024 was higher than Shein's, at 54% versus 36%. This is likely due to Vinted’s relative novelty in e-commerce. Shein has been active in the market for several years and ranks third in fashion, while Vinted ranks fifth.

TikTok Shop is not as high in fashion GMV, with US$654 million, but it has a high growth rate of 66%. However, no one beats Temu in terms of growth; it increased its revenues by 285% from 2023 to 2024. With a GMV of $1.4 billion, Temu ranks tenth in UK fashion.

Legacy Fast-Fashion Brands Face Consequences of Market Shifts

The real losers in this game are the fashion platforms that fail to differentiate themselves. Their similar low-cost, fast-turnover strategies put customers at a crossroads: Should they buy from Temu, Shein, Vinted, or TikTok Shop? Or should they buy from River Island, ASOS, Boohoo, PrettyLittleThing, or Zalando.co.uk? More and more, the balance skews toward the former.

Boohoo and Prettylittlething saw declines of -20% and -19%, respectively. River Island experienced degrowth of -18% from 2023 to 2024, while Zalando.co.uk saw a -17% loss in revenue. Asos fell by -13%.

In addition, none of their GMVs are competitive, ranging from US$208 million for Boohoo to US$321 million for River Island. Only Asos stands out, with a GMV of US$1.2 billion, placing it 12th in UK fashion, behind Temu in 10th place.

The competition is intense, so even formerly leading fast-fashion brands are struggling to remain in the upper market tiers.

Next, Uniqlo, H&M and Zara Drop to Middle Market Tier

Next and Uniqlo are in the middle tier. They grew at respective rates of 8% and 16% from 2023 to 2024. With a GMV of US$1.9 billion in 2024, Next is one of the biggest fashion retailers in the market. Next ranks sixth in UK fashion e-commerce, while Uniqlo is still ascending and generating only a smaller GMV of US$323.8 million.

Therefore, Uniqlo is in a slightly more optimistic position than H&M, which stagnated at a growth rate of -1% and generated US$326.4 million in UK e-commerce. Its closest competitor Zara is more successful with a GMV of US$662.4 million and a growth rate of 11%.

Market Shifts Reveal Challenges for Traditional Fast-Fashion

UK fashion e-commerce is undergoing a change. Consumers favor affordability, wide product ranges and social integrations over the traditional model. The market shifts are the reasons why traditional fast-fashion brands are losing ground. Only the ones with a refined brand identity, seamless online experience and consumer recognition maintain their leading positions in the market.