May E-Commerce Update: Global Online Retail Reaches US$430 Billion

May 2026 showed stable growth compared to last year, at an increase of 9.3%. Here are the countries and categories behind this development.

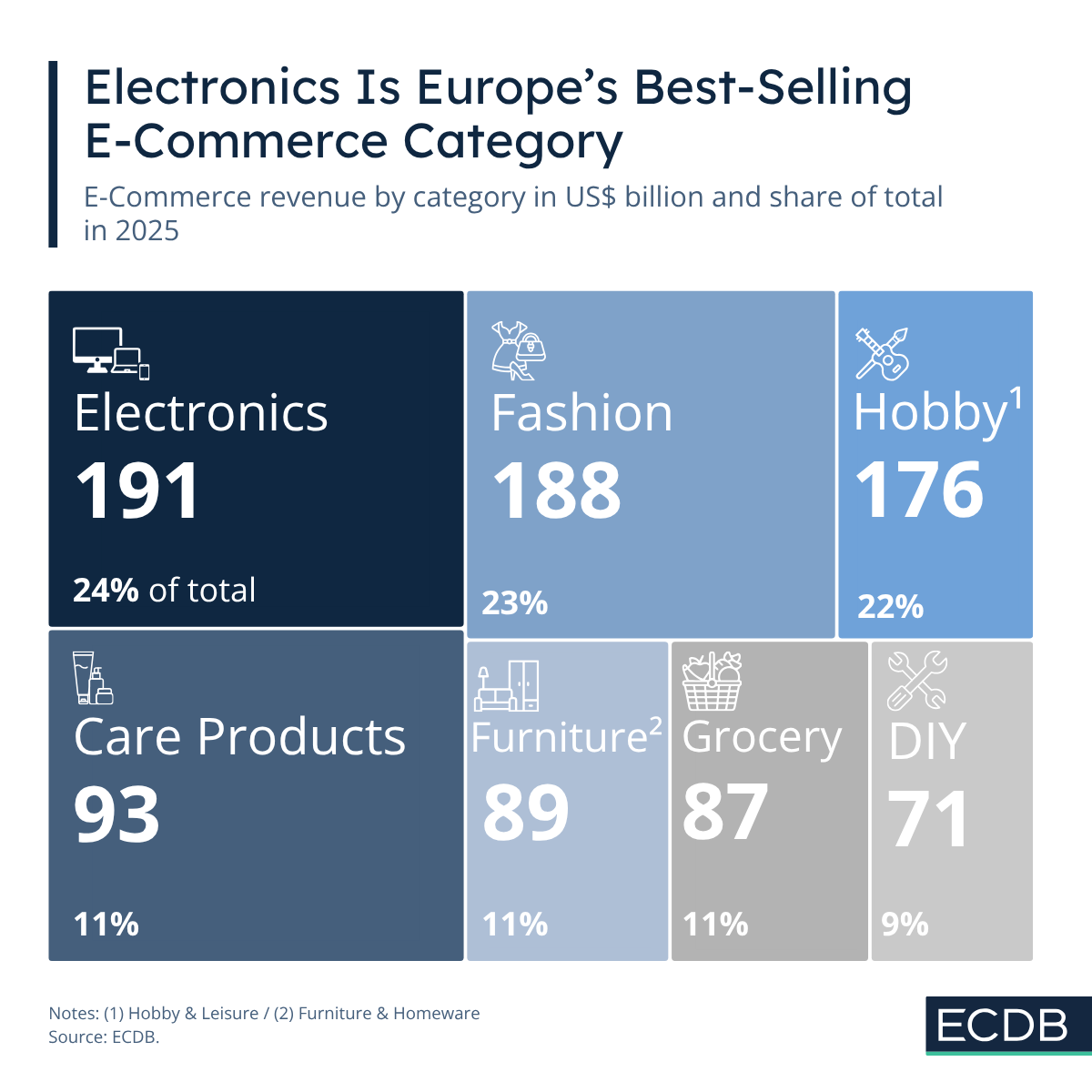

European Category Treemap

Electronics is Europe's best-selling e-commerce category, but the other categories are not far off. Here are the categories that are leading, and the ones that drive e-commerce expansion forward.

Nadine Koutsou-Wehling

Data Journalist

June 03, 2026

Market Trends

European e-commerce reaches a total GMV of US$791 billion in 2025. The distribution of category spend reveals a clear hierarchy, which is discussed in the following.

At the top of the market sits Electronics, generating US$191 billion in revenue, which accounts for 24% of total European e-commerce GMV.

A key driver of this dominance is the internal structure of the category:

Consumer Electronics accounts for 65% of all Electronics revenue

Continued demand for smartphones, laptops, smart devices, and gaming hardware continues to anchor growth

Several structural advantages reinforce Electronics’ leadership position:

Wide assortment availability across price tiers and brands

Deep marketplace penetration, especially via large multi-category platforms

Stable cross-border demand, with consumers frequently purchasing from outside domestic markets

High Net Average Order Value (AOV) of US$137.5 globally

In second place is Online Fashion, generating US$188 billion, or 23% of total market revenue.

Despite being slightly smaller than Electronics, Fashion remains one of the most competitive categories in European e-commerce.

Its internal breakdown shows clear consumer priorities:

Apparel: 59% of Fashion revenue

Footwear: 22%

Bags & Accessories: 19%

Footwear and Bags & Accessories can be seen as more complementary revenue drivers than apparel, which has a broad appeal for online shopping across the continent.

Ranking third is Hobby & Leisure, with US$176 billion in revenue in 2025.

What makes this category especially notable is its balanced internal composition:

One third is made up of Media

The second third includes Other segments (collectibles, model kits and drones)

The remaining third encompasses Toys, Stationery, Crafts & Art Supplies, as well as Sports Equipment

A wide definition of the category and increasing online shopping on entertainment, personalization and niche interests makes Hobby & Leisure the third largest category in European e-commerce.

Beyond the top three, several major categories show the direction in which European e-commerce is moving:

Care Products: US$93 billion

Furniture & Homeware: US$89 billion

Grocery: US$87 billion

DIY: US$71 billion

These categories are especially important because they represent the normalization of online shopping for everyday and traditionally offline-heavy purchases.

European e-commerce in 2025 is defined by a clear duality between mature, high-value digital retail categories and the accelerating digitization of everyday consumption. At the top of the market, Electronics and Fashion together account for nearly half of total GMV. At the same time, the most important structural shift in the market is the steady rise of everyday essentials in e-commerce. Categories such as Grocery and Care Products are increasingly central to growth dynamics. Their expansion reflects a deeper behavioral change in which consumers are progressively moving routine and replenishment-driven purchases online.

Related Articles

May 2026 showed stable growth compared to last year, at an increase of 9.3%. Here are the countries and categories behind this development.

The Nordics are among the most digitally advanced regions in the world, with internet penetration exceeding 98%. Yet the size of the e-commerce market remains limited. This is primarily due to structural factors and the smaller population size of each individual market.

Temu, TikTok and Shein are known for their low cost and high product variety: Here is proof that they are primarily used by younger shoppers. But exceptions remain.

Click here for

more relevant insights from

our partner Mastercard.

Our Tool

We’re not just another blog—we’re an advanced e-commerce data analytics tool. The insights you find here are powered by real data from our platform, providing you with a fact-based perspective on market trends, store performance, industry developments, and more.

Analyze retailers in depth with our extensive Retailer dashboards and compare up to four retailers of your choice.

Learn More

Combine countries and categories of your choice and analyze markets in depth with our advanced market dashboards.

Learn More

Compile detailed rankings by category and country and fine-tune them with our advanced filter options.

Learn More

Discover relevant leads and contacts in your chosen markets, build lists, and download them effortlessly with a single click.

Learn More

Benchmark transactional and conversion funnel KPIs against market standards and gain insight into the key metrics of your relevant market.

Learn MoreOur reports provide pre-analysed data and highlight key insights to help you quickly identify key trends.

Learn More

Book a demo to see how ECDB's market intelligence can support your business.