Amazon's Competitive Advantage Is the Number of Times Customers Return

The average customer buys 19.5 times a year at Amazon, much more often than at its competitors. What factors bring customers back to the site that often?

E-Commerce Omnichannel

Walmart's online sales grew 35% last year by leaning on the thing e-commerce-only brands don't have: 4,600 physical stores. Here's what that looks like in the data, and where it goes wrong.

Nadine Koutsou-Wehling

Data Journalist

July 15, 2026

Transactions

Article in a Nutshell:

Walmart's online GMV grew 35.09% in 2025, one of the fastest growth rates of any major retailer, built on using its stores as pickup points and mini warehouses, not just legacy overhead.

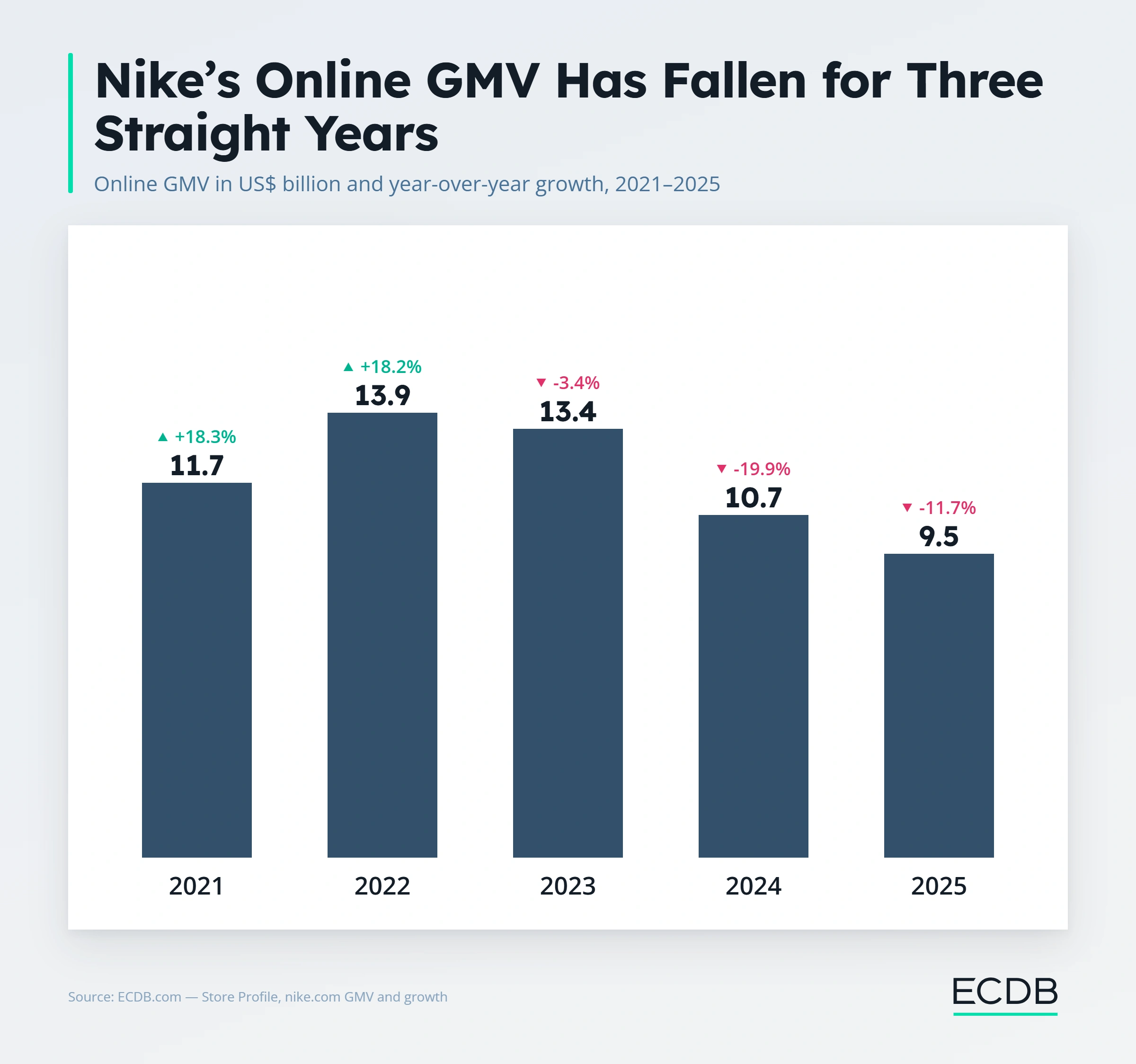

Nike, once the industry's model direct-to-consumer story, saw online GMV fall 11.69% in 2025, proof that building an omnichannel strategy once doesn't mean it keeps paying off.

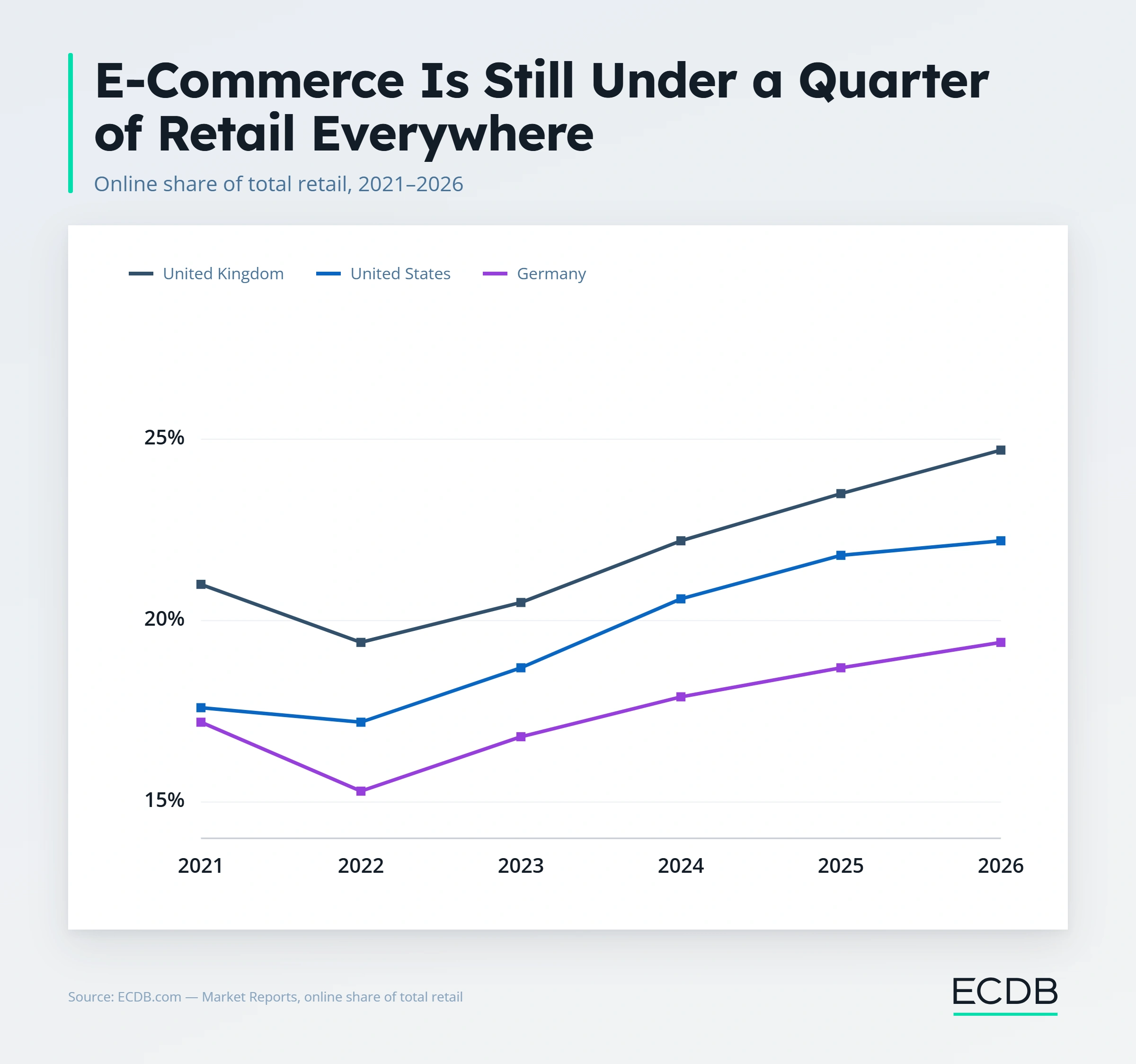

Online sales are still just 18.69% to 23.43% of total retail in the US, Germany, and the UK, so even the most digitally mature markets are still mostly offline. That gap is exactly why omnichannel exists.

Omnichannel means selling through more than one channel: Online store, physical stores, an app, a marketplace, and making those channels work together instead of competing for the same sale.

A customer should be able to check stock online, buy in an app, and return in a store without the brand treating those as three separate businesses. The real-world data on retailers that do this well, and one that's currently struggling with it, shows what actually separates the two.

Even in the world's most developed e-commerce markets, online is still a minority of total retail spending. In the US, e-commerce is 21.71% of retail. In the UK, 23.43%. In Germany, 18.69%. That means somewhere between three-quarters and four-fifths of retail spending in these countries still happens offline.

A brand that only sells online is capping itself to a fifth of the market at best. A brand that only sells in stores is missing the fastest-growing slice. Omnichannel is merely a response to the fact that neither channel alone covers where people actually spend money.

Walmart's online business grew 35.09% in 2025, reaching US$170.4 billion in online GMV, the fastest growth of any retailer in this comparison by a wide margin. That growth is happening exactly because of Walmart's roughly 4,600 US stores: Stores double as fulfillment points for pickup and fast local delivery. They turn what could be a fixed cost into a same-day delivery advantage that a warehouse-only competitor can't easily match.

Walmart also runs as a Hybrid store, selling its own inventory alongside third-party marketplace sellers on walmart.com. That adds a second kind of channel expansion on top of the store network: more assortment without Walmart having to hold the inventory itself.

Target runs a similar model, using stores for pickup and fast delivery, and is also a Hybrid store mixing its own inventory with marketplace sellers.

But its online growth, 5.23% in 2025, is a fraction of Walmart's. The playbook is the same. The size is not. With fewer stores and less density than Walmart, Target gets a smaller version of the same advantage, a reminder that omnichannel's payoff grows with how much physical footprint a brand actually has to work with.

Sephora's version of omnichannel is about experience: letting a customer get color-matched, try a product, and get advice in store, then buy there or finish the purchase online later.

Sephora sells only its own inventory online, no marketplace layer, and its online GMV still grew 10.12% in 2025. The channel advantage here is that the in-store experience makes the online purchase easier to commit to, which is a different route to the same result: channels reinforcing each other instead of competing.

Nike spent years as the industry's reference case for direct-to-consumer, building its own stores, its own app, and its own online channel to reduce reliance on wholesale partners. More recently, Nike has leaned back into wholesale relationships it had pulled away from. Its online GMV fell 11.69% in 2025, the steepest decline of any retailer in this comparison.

That's the caution this article opened with: an omnichannel strategy isn't a one-time build. Nike didn't lose its stores, its app, or its website, it changed how much weight its own direct channel was given relative to partners, and the online numbers moved with that decision.

Building the channels is the first step. Continuing to invest in coordinating them is the part that doesn't stay finished.

Not every omnichannel retailer is accelerating or declining sharply, and steady is still a legitimate outcome.

Best Buy's online GMV grew just 1.34% in 2025, essentially flat.

IKEA grew 8.79%, solid but unspectacular.

Both sell only their own inventory online, and both lean on their stores for showrooming, returns, and pickup rather than headline-making growth.

For categories like electronics and furniture, where customers often want to see or test a product before buying, that steady coordination between channels is doing its job even when the growth chart doesn't look dramatic.

The retailers whose online channel is accelerating, Walmart, Sephora, and IKEA, are the ones still actively using their physical footprint or in-store experience as part of the sale, not treating stores as a separate, legacy business.

Nike's decline shows the flip side: the same company, the same stores, the same app, but less weight put on the direct channel, and the online numbers reflect that shift directly.

Omnichannel is a balance that has to keep being actively managed.

Every number in this article, GMV, growth, and store type, comes from ECDB's tracking of these retailers' online channels specifically, alongside thousands of others across markets and categories. That data makes it possible to see a shift like Nike's pullback or Walmart's acceleration in the numbers directly, rather than waiting for it to become a headline.

Customers use this in a few concrete ways: tracking a retailer's online growth over time to catch a channel strategy working or slipping early, checking whether a retailer has added a marketplace layer (the store type field) to see how its assortment strategy is evolving, and benchmarking a retailer's online performance against competitors before deciding where to put the next investment, in stores, in an app, or in the online channel itself.

That data is available through ECDB's Profiles and Rankings tools for any retailer worth tracking.

Related Articles

The average customer buys 19.5 times a year at Amazon, much more often than at its competitors. What factors bring customers back to the site that often?

Cross-selling is one of those e-commerce strategies used to improve e-commerce sales. But for whom does it make sense? Which other strategies are aligned with it?

Launching new products too often relies on hunches and guesswork than traceable market data. ECDB provides the answer based on real-time e-commerce market intelligence.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.