June 2026 E-Commerce Recap: US$436.8 Billion in Global Revenue

The start of summer brought positive developments in June, with US$436.8 billion in global e-commerce revenues and a 9.5% year-on-year increase. Read on for the details here.

Shifting Global Growth Patterns

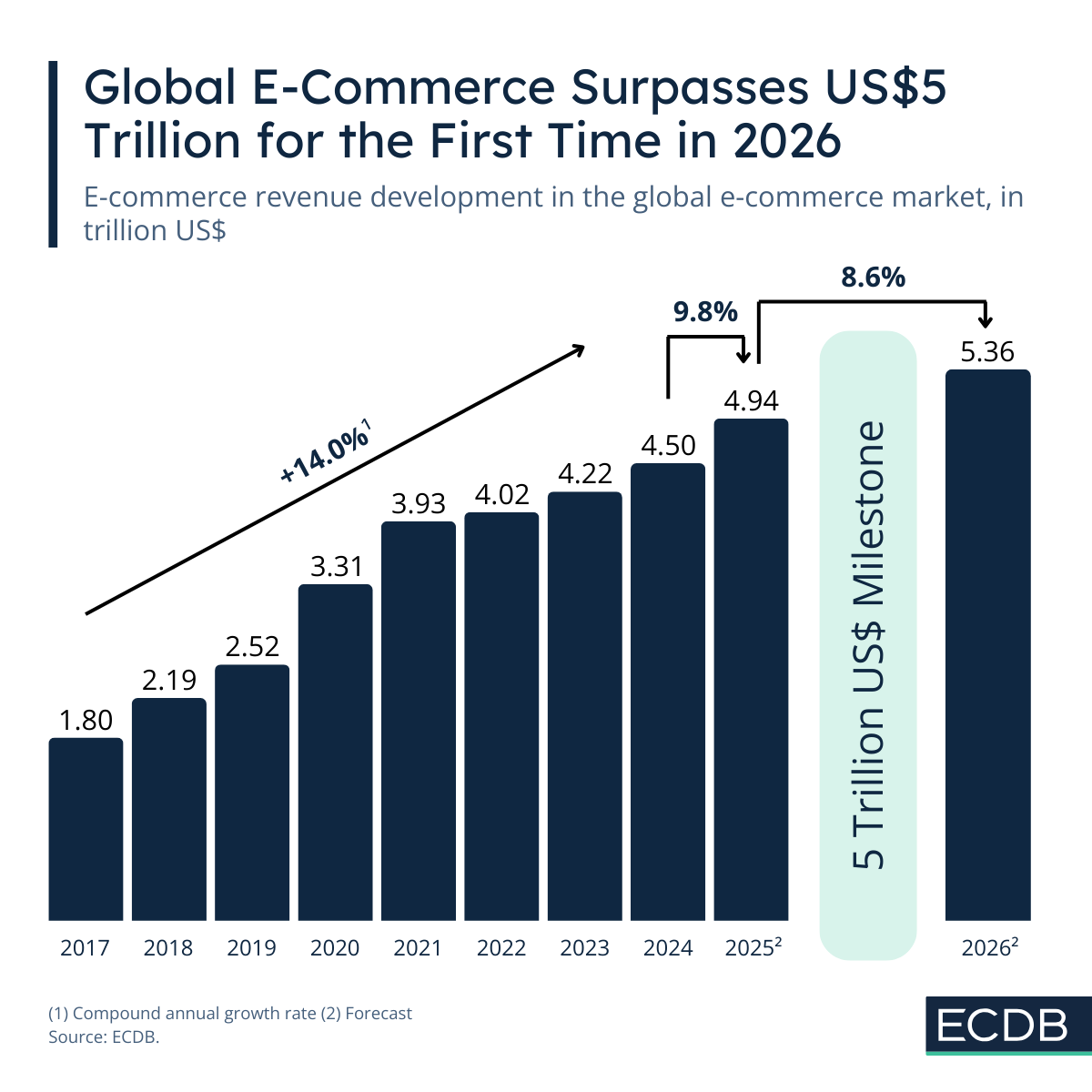

The global e-commerce market reaches a historic milestone in 2026, surpassing US$5 trillion for the first time. Yet while the world celebrates record scale, growth becomes increasingly uneven: Latin America accelerates, GSA stalls, and category dynamics shift—most notably with grocery surpassing a 10% share for the first time. At the same time, major retail giants face pressure, while TikTok Shop emerges as one of the fastest-growing platforms worldwide.

David Niemeier

November 18, 2025

Market Trends

Article in a Nutshell:

Global e-commerce exceeds US$5 trillion in 2026.

Latin America leads all regions with 12.4% growth; GSA trails at 4.6%.

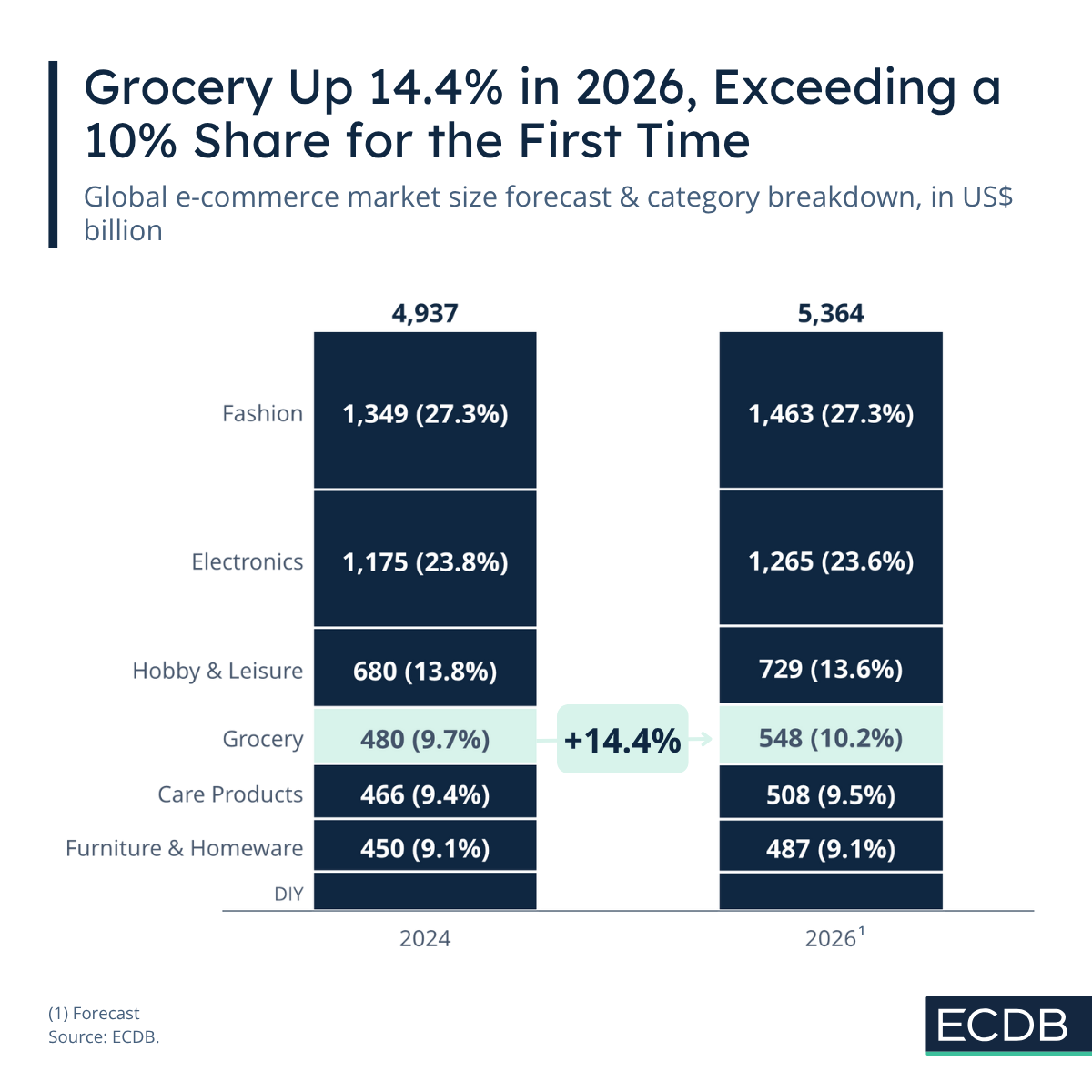

Grocery grows 14.4%, surpassing a 10% market share.

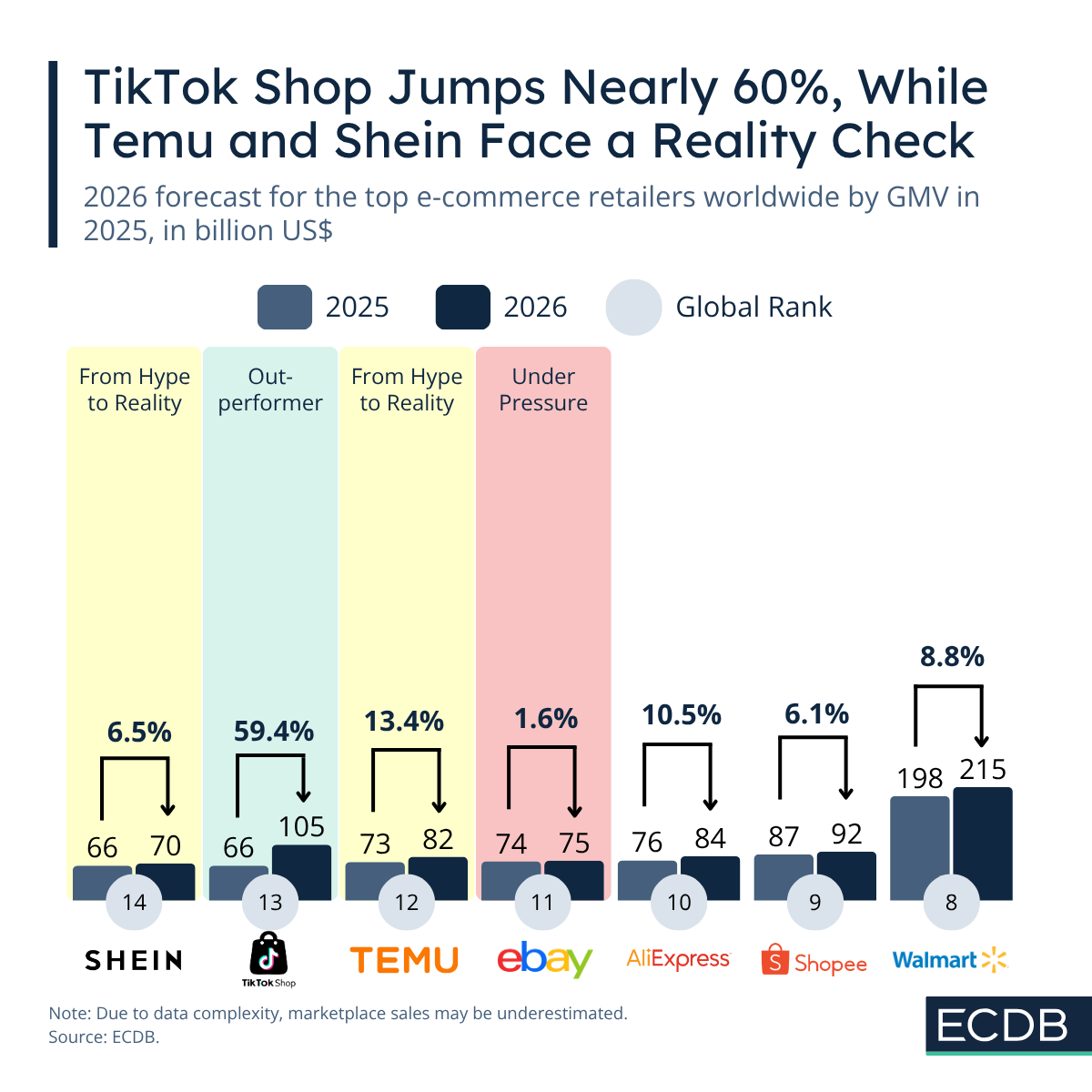

Multiple top global retailers stagnate or decline—while TikTok Shop jumps nearly 60%.

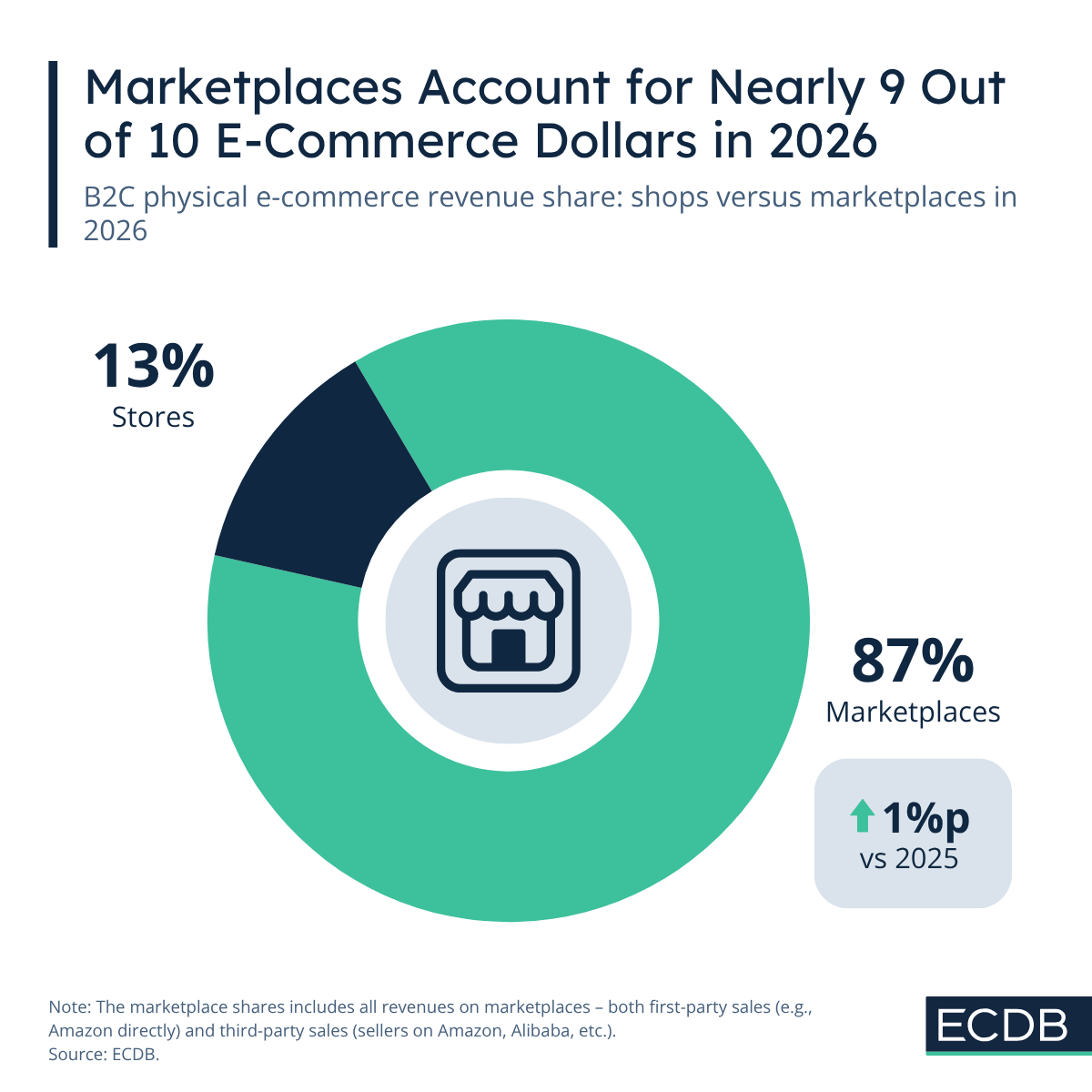

Marketplaces are responsible for 87% of global online spending.

After years of steady expansion, 2026 marks a historic moment: global e-commerce revenue surpasses the US$5 trillion threshold. While growth has moderated since the pandemic highs, the market continues to expand at a healthy pace—driven by rising adoption, improved logistics, and the continued shift from offline to online across emerging markets.

2026 highlights a clear divergence across regions. Latin America emerges as the world’s fastest-growing e-commerce region, significantly outperforming the global average.

Meanwhile, the GSA region (Germany, Switzerland, Austria) registers the weakest growth among major economic blocs.

Grocery continues to be one of the strongest growth drivers globally. In 2026, it surpasses a 10% share of global e-commerce revenue—an important structural shift that reflects broader adoption, improved delivery reliability, and new quick-commerce hybrid models.

TikTok Shop emerges as one of the fastest-growing global eCommerce players, expanding its GMV by nearly 60% in 2026.

The platform’s hybrid model—fuelled by algorithmic discovery, livestream selling and aggressive merchant incentives—continues to outperform expectations.

Meanwhile, Shein and Temu encounter cooling momentum. Growth slows significantly, signaling a shift from hyper-expansion to more sustainable, moderated trajectories.

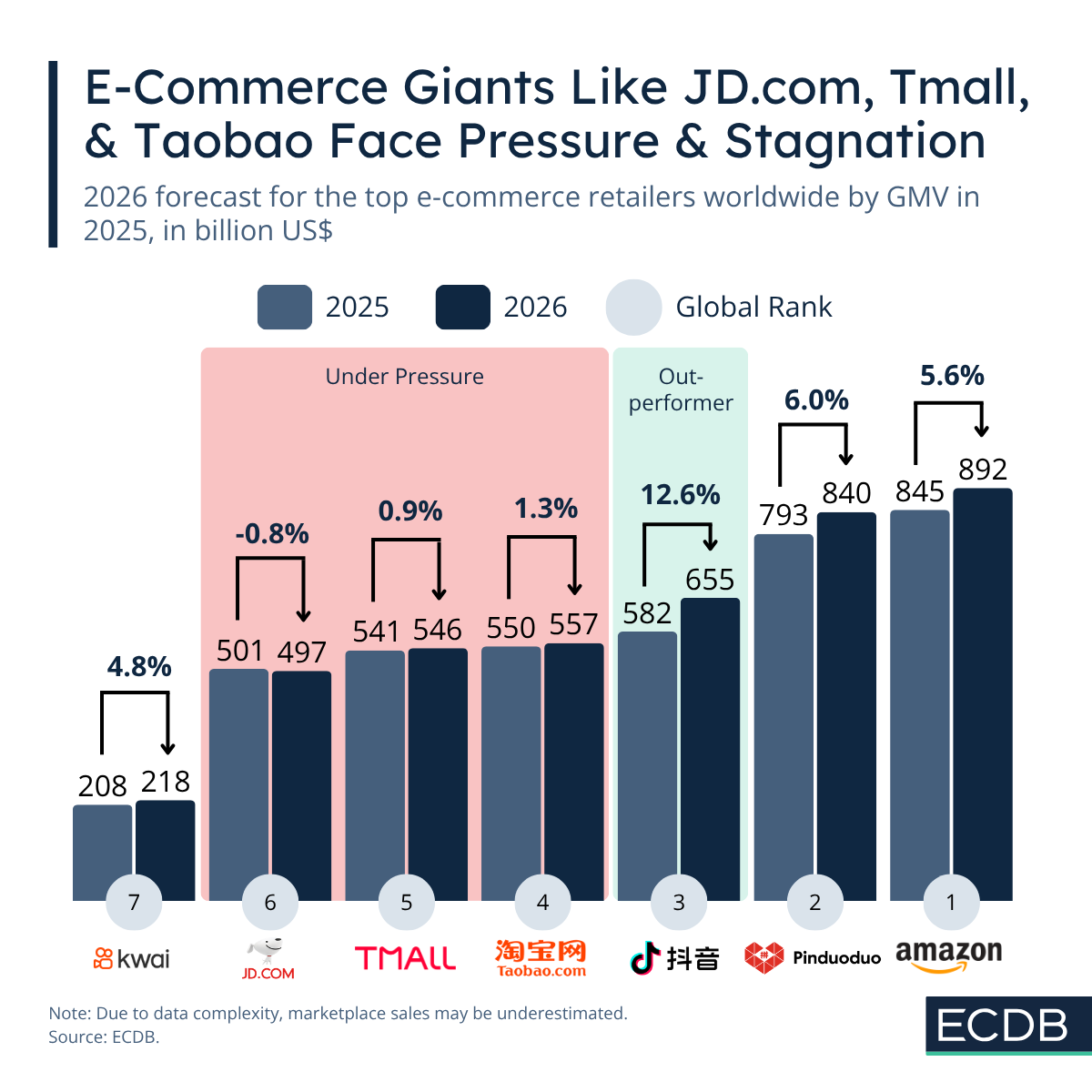

Amid slowing global growth, multiple top retailers experience stagnation or even mild decline.

JD.com contracts. Tmall and Taobao grow only marginally. Pinduoduo and Amazon continue expanding, though at moderate rates. TikTok Shop stands out as the clear outperformer.

The marketplace model continues its global dominance.

By 2026, 87% of all B2C physical e-commerce spending flows through marketplaces—up 1 percentage point from 2025.

This reflects expanding seller ecosystems, platform-native advertising, and the continued rise of social-commerce-driven marketplaces.

The global e-commerce landscape in 2026 tells a story of scale—and divergence.

Milestones are reached, but growth is shifting toward regions and categories that bled affordability, convenience and digital maturity. Platforms like TikTok Shop disrupt traditional players, while some of the world’s largest retailers face stagnation in a cooling competitive environment.

As the world moves into 2027, the defining question becomes how quickly retailers can adapt to uneven regional dynamics, platform concentration and evolving consumer behavior.

Those who invest in agility, cross-border capability, marketplace excellence and new commerce experiences will be best positioned to lead the next phase of global digital retail.

Related Articles

The start of summer brought positive developments in June, with US$436.8 billion in global e-commerce revenues and a 9.5% year-on-year increase. Read on for the details here.

Central Europe is dominated by one market in particular: Germany. The others follow at a far distance. They include Poland, Austria, Switzerland, and Greece. Here is how they compare.

In Italy, 66% of the top 250 online store's net sales are generated by the top 5. This makes it the most concentrated market among the EU-Big Five. What does that mean for e-commerce? Find it out here.

Click here for

more relevant insights from

our partner Mastercard.

Book a demo to see how ECDB's market intelligence can support your business.